Market Insights: Volatility Declining at the Same Time as Stocks Offers Optimism

Milestone Wealth Management Ltd. - Mar 21, 2025

Macroeconomic and Market Developments:

- North American markets were up this week. In Canada, the S&P/TSX Composite Index rose 1.69%. In the U.S., the Dow Jones Industrial Average advanced 1.20% and the S&P 500 Index increased 0.51%, finally ending a four-week losing streak.

- The Canadian dollar was slightly higher, closing at 69.7 cents vs 69.6 cents USD last week.

- Oil prices were up this week. U.S. West Texas crude closed at US$68.28 vs US$67.19 last week.

- The price of gold rose again this week to another all-time high, closing at US$3,021 vs US$2,993 last week.

- The Bank of Canada Governor Tiff Macklem signaled a new approach to interest rate policy, as tariff uncertainty and global trade tensions cloud the economic outlook. While Canada began 2025 in solid shape, Macklem warned that a prolonged trade war with the U.S. and China could trigger a recession, prompting the central bank to prepare a range of economic scenarios rather than a single forecast. With inflation at 2.6% and potentially rising due to tariffs, Macklem stressed the need for flexibility and faster policy responses, noting that monetary policy can’t fully offset trade war impacts.

- CIBC Capital Markets says a softer U.S. dollar is likely to boost earnings for Canadian firms with significant foreign revenue, as 60% of TSX-listed companies' sales are booked in non-Canadian currencies. Analyst Ian de Verteuil also points to rising gold prices and speculation around a possible “Mar-a-Lago Accord” aimed at devaluing the greenback, making the S&P/TSX well-positioned for upside, particularly among globally diversified firms reporting in CAD.

- Hudson’s Bay Co. has received court approval to begin liquidating 90 of its 96 stores starting Monday, with only six locations—primarily in Toronto and Montreal—temporarily spared as discussions with landlords continue. The iconic retailer is exploring a last-ditch restructuring, but no agreement is in place. The closures could impact over 9,000 employees and significantly alter mall traffic dynamics across Canada. Despite strong recent sales, HBC still faces major financial hurdles, including a $7 million monthly payment to joint-venture partner RioCan.

- Facing potential Trump administration tariffs on foreign auto imports, Audi is exploring plans to move vehicle production to the U.S., aiming to be closer to American consumers and mitigate global economic risks. While no final decision has been made, the company expects to announce its U.S. market production plans later this year—a significant pivot for the German automaker, which currently builds key models like the Q5 in Mexico.

- In the U.S. Retail sales rose just 0.2% in February, falling short of the expected 0.6% gain, with last month’s figures revised lower. The headline increase was driven almost entirely by online sales (+2.4%), while restaurant and bar sales fell sharply (-1.5%), hinting at softening demand for services. Core retail sales (excluding autos, gas, and building materials) rose 0.5%, but only 0.1% including revisions, pointing to a flat Q1 if March is unchanged. Inflation-adjusted sales are barely positive year-over-year, reinforcing ongoing pressure on consumer purchasing power.

Weekly Diversion:

Check out this video: Let the madness begin

Charts of the Week:

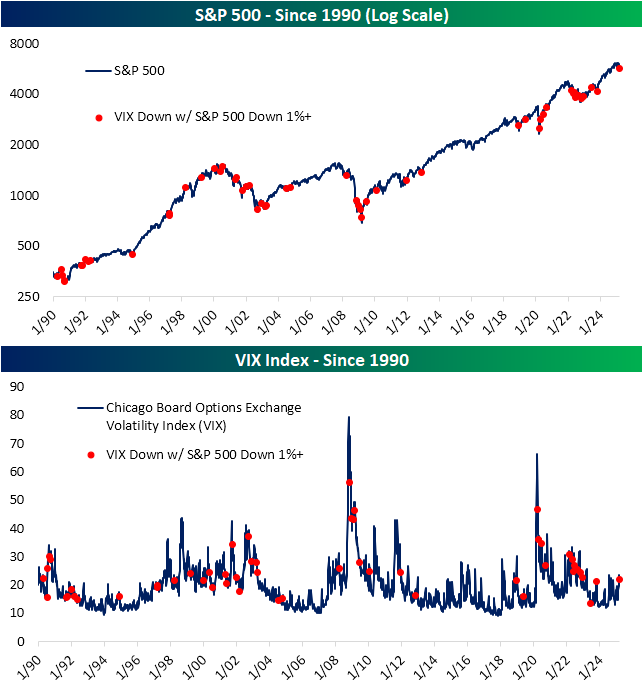

Last week, the S&P 500 declined by over 1% while the CBOE Volatility Index (VIX) also decreased. This pattern is relatively uncommon, occurring only about 2.9% of the time since 1990. The VIX is a popular measure representing the market’s expectations for the relative strength of near-term price changes of the S&P 500 Index. Volatility is often seen to gauge market sentiment, and particularly the degree of fear among market participants. Therefore, a lower or declining VIX is viewed as a positive. The following charts of the S&P 500 and VIX Indices show these points in time when the VIX was down, and the S&P 500 was down over 1% in the same week.

Source: Bespoke Investment Group

Historically, these instances have been observed in various stages of the market cycle. While there hasn’t been a perfectly clear pattern of when this occurs (bull or bear market), they do tend to precede stronger forward-looking returns for the S&P 500 Index on average, offering some optimism.

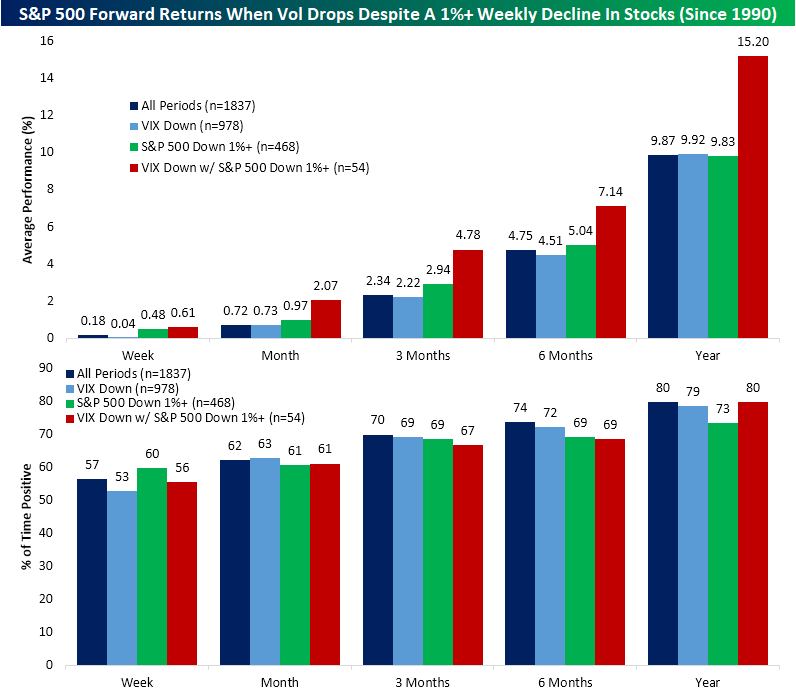

The next chart illustrates the S&P 500's various forward-looking returns following these occurrences (red bar) compared to only when the S&P is down over 1% or to only when the VIX is down in a week, as well as all periods. As one can see, the red bars on the first chart are significantly higher on average than the other periods. It is important to note the very strong out performance one year later, with the average return after these instances being over 50% more than the other periods. Taking all together, this suggests that while these events are not necessarily consistent in terms of when they occur, they do tend to be associated with much better than average forward-looking returns.

Source: Bespoke Investment Group

Sources: Yahoo finance, First Trust, Bloomberg, Breitbart, Richardson Wealth, Bespoke Investment Group

©2025 Milestone Wealth Management Ltd. All rights reserved.

DISCLAIMER: Investing in equities is not guaranteed, values change frequently, and past performance is not necessarily an indicator of future performance. Investors cannot invest directly in an index. Index returns do not reflect any fees, expenses, or sales charges. Opinions and estimates are written as of the date of this report and may change without notice. Any commentaries, reports or other content are provided for your information only and are not considered investment advice. Readers should not act on this information without first consulting Milestone, their investment advisor, tax advisor, financial planner or lawyer. This communication is intended for Canadian residents only and does not constitute as an offer or solicitation by anyone in any jurisdiction in which such an offer is not allowed.