Market Insights: Using Valuations to Cut Through the Noise

Milestone Wealth Management Ltd. - Mar 14, 2025

Macroeconomic and Market Developments:

- North American markets were down again this week. In Canada, the S&P/TSX Composite Index fell slightly 0.83%. In the U.S., the Dow Jones Industrial Average fell 3.07% and the S&P 500 Index was down 2.27%.

- The Canadian dollar remained relatively stagnant this week, closing at 69.6 cents vs 69.5 cents last week.

- Oil prices avoided falling again this week. U.S. West Texas crude closed at US$67.19 vs US$67 last week.

- The price of gold reached new all-time highs this week, at one point tipping over $3,000 intraday, closing at US$2,993 vs US$2,917 last week.

- The Bank of Canada lowered rates by 25bps, citing heightened US-Canada trade tensions, which are expected to slow economic activity and drive inflation higher. While inflation remains near the 2% target, the end of the GST holiday is projected to push CPI to 2.5% in March. The BoC warned that tariff uncertainty is restraining consumer spending, business hiring, and investment, but emphasized that monetary policy cannot offset trade war impacts—only prevent inflation from becoming entrenched.

- Whitecap and Veren have entered a $15 billion all-share merger, forming the largest Canadian light oil-focused producer with a combined 370,000 boe/d production. The deal is expected to close by May 30, 2025, with Whitecap shareholders owning 48% and Veren shareholders 52%. The merger is projected to generate $200M in annual synergies, boost free funds flow per share by 26%, and increase Veren shareholders' dividend by 67%.

- In the U.S. the Senate Banking Committee approved the GENIUS Act, a bipartisan Digital Asset bill establishing a regulatory framework for stablecoins, with Federal Reserve oversight for large issuers. The panel also advanced the FIRM Act, which seeks to prevent financial institutions from using reputational risk to justify debanking. While the GENIUS Act passed with bipartisan support (18-6 vote), the FIRM Act advanced on a party-line 13-11 vote, reflecting ongoing political divisions over financial regulation.

- Consumer prices rose 0.2% in February, coming in below expectations (0.3%), with annual inflation easing to 2.8%. Core CPI (excluding food and energy) also increased 0.2%, bringing the yearly rate to 3.1%, still above the Fed’s 2.0% target. Housing rents remain a key driver of inflation, while “Supercore” inflation—closely watched by the Fed—rose 3.8% year-over-year. While the data shows modest improvement, inflation remains elevated, making a near-term rate cut unlikely.

- The Producer Price Index (PPI) was unchanged in February, coming in below expectations (0.3%), but annual producer inflation remains elevated at 3.2%. Core PPI (excluding food and energy) fell 0.1% but is up 3.4% year-over-year, reflecting an accelerating trend from 2024 levels. Large category swings—a 53.6% spike in egg prices offset by a 1.2% drop in energy—masked underlying price pressures. With trade uncertainty adding volatility to supply chains, inflation risks persist, keeping Fed rate cut expectations in check.

Weekly Diversion:

Check out this video: Maybe once I control my slice

Charts of the Week:

In the current volatile financial markets, it's easy to get caught up in the daily noise of economic data, central bank announcements, and earnings reports. However, focusing on long-term investing goals and understanding valuations can provide a crucial perspective that helps keep portfolios grounded amidst uncertainty.

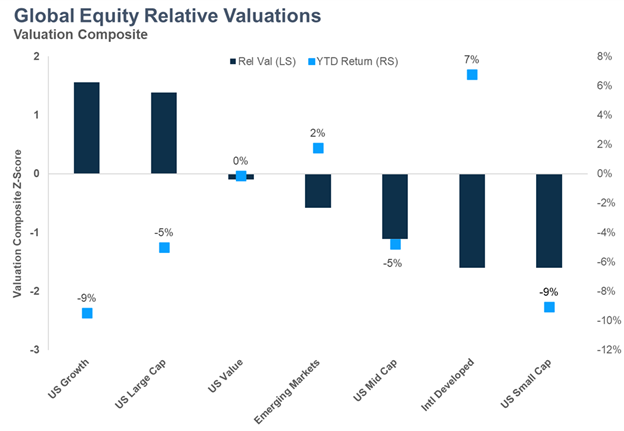

Currently, growth stocks, which make up a significant portion of the U.S. large cap market, remain relatively expensive compared to U.S. small and mid-cap stocks and developed international markets, as shown in the chart below. We say ‘expensive’ with a grain of salt here as there is a valid reason why some companies have higher valuations. It's because they have grown rapidly in the past and are expected to keep growing strongly. This is why the U.S market is valued relatively higher. These valuation differences are not a timing mechanism and can persist for years or even decades. As investors reassess future growth prospects, companies with high growth expectations—and thus higher valuations—have seen their prices adjust more quickly. This has been particularly evident in the recent correction of richly priced technology sectors.

Source: Carson Investment Research, Morningstar Direct - Valuations as of 02/28/2025, Returns as of 03/12/2025

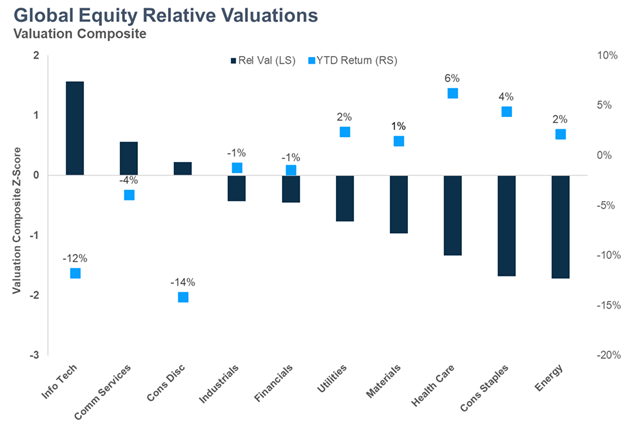

Interestingly, while defensive sectors are often expected to perform well during market corrections, cyclical sectors tied to economic growth have also held up relatively well, as highlighted in the next chart. This resilience might be attributed to their valuation cushion, among other factors. The dynamic between these sectors highlights the importance of valuations in navigating market fluctuations.

Source: Carson Investment Research, Morningstar Direct - Valuations as of 02/28/2025, Returns as of 03/12/2025

Valuations may change slowly compared to daily market fluctuations, but they offer an important long-term perspective. By regularly examining valuation metrics such as Price-to-Earnings (P/E), Price-to-Book (P/B), and Price-to-Sales (P/S) ratios, investors can make more informed long-term decisions and maintain a level head during market volatility. Whether navigating economic shifts or seeking stability, valuations are an essential tool for cutting through the noise and staying focused on investment goals.

Sources: Sources: Yahoo finance, First Trust, Bloomberg, Fox Business, Richardson Wealth, Canaccord Genuity Wealth, Carson Investment Research, Morningstar Direct

©2025 Milestone Wealth Management Ltd. All rights reserved.

DISCLAIMER: Investing in equities is not guaranteed, values change frequently, and past performance is not necessarily an indicator of future performance. Investors cannot invest directly in an index. Index returns do not reflect any fees, expenses, or sales charges. Opinions and estimates are written as of the date of this report and may change without notice. Any commentaries, reports or other content are provided for your information only and are not considered investment advice. Readers should not act on this information without first consulting Milestone, their investment advisor, tax advisor, financial planner or lawyer. This communication is intended for Canadian residents only and does not constitute as an offer or solicitation by anyone in any jurisdiction in which such an offer is not allowed.