Market Insights: Ignoring Market Noise: Staying Invested for the Long-Term

Milestone Wealth Management Ltd. - Mar 07, 2025

Macroeconomic and Market Developments:

- North American markets were down this week. In Canada, the S&P/TSX Composite Index declined 2.50%. In the U.S., the Dow Jones Industrial Average was down 2.37% and the S&P 500 Index fell 3.10%.

- The Canadian dollar rose slightly this week, closing at 0.69.5 cents vs 69.1 cents USD last week.

- Oil prices fell again this week. U.S. West Texas crude closed at US$67 vs US$69.75 last week.

- The price of gold increased this week, closing at US$2,917 vs US$2,856 last week.

- Canada added just 1,100 jobs in February, well below the 20,000 expected, as tariff uncertainty and harsh winter weather weighed on hiring. The unemployment rate held steady at 6.6%, but weak job growth pushed market odds of a Bank of Canada rate cut next week to 85%. While employment increased in retail, finance, and real estate, declines in scientific, technical, and transportation sectors highlight uneven labor market conditions.

- Canada and Mexico received a temporary exemption from President Trump’s 25% tariffs under the USMCA, pushing implementation to April 2. While auto parts meeting USMCA rules remain tariff-free, sectors like Canadian potash and energy face lower but still significant tariffs. The exemptions are tied to efforts on fentanyl and immigration.

- President Trump signed an executive order creating a Strategic Bitcoin Reserve, using 200,000 government-owned bitcoins from forfeitures as a store of value with no cost to taxpayers. The order also establishes a U.S. Digital Asset Stockpile, including other seized cryptocurrencies like XRP, Solana (SOL), and Cardano (ADA). Crypto Czar David Sacks praised the move, arguing that premature bitcoin sales have already cost taxpayers $17 billion in lost value and that this policy aims to maximize U.S. crypto holdings.

- OPEC+ will raise output by 138,000 barrels per day in April, following pressure from President Trump to bring down oil prices and offset inflationary effects from tariffs. Brent crude dropped 2.8% to a three-month low after the announcement. While Saudi Arabia and Russia lead the decision, the move also benefits Russia amid U.S. sanctions and aligns with Washington’s tighter restrictions on Iranian exports. Global markets were already facing a supply surplus, adding further downward pressure on oil prices.

- The ISM Non-Manufacturing Index rose to 53.5 in February, exceeding expectations and signaling continued growth in the service sector, which drives two-thirds of the U.S. economy. Employment hit its highest level since 2021.

- The U.S. economy added 151,000 jobs in February, falling short of expectations, while unemployment rose to 4.1%. Job gains were strongest in healthcare (+52K), financial activities (+21K), and transportation (+17.8K), while federal employment declined by 10K due to DOGE-led cuts. The weaker-than-expected report reinforced market expectations that the Fed will keep rates steady in March, as policymakers balance slowing job growth against lingering inflation risks.

Weekly Diversion:

Check out this video: I may have to get a Golden Retriever now

Charts of the Week:

North American Markets have an elevated level of volatility year-to-date with the S&P 500 Index and Nasdaq Composite down 1.94% and 6.08%, respectively, while our S&P/TSX Composite down just 0.04%. Much of this volatility has to do with trade-related decisions by U.S. leadership including tariffs. However, as the following charts illustrate, staying invested over the long-term through compound growth is a crucial strategy for achieving financial success and securing a stable financial future regardless of administrations, bull and bear markets, and major economic headwinds.

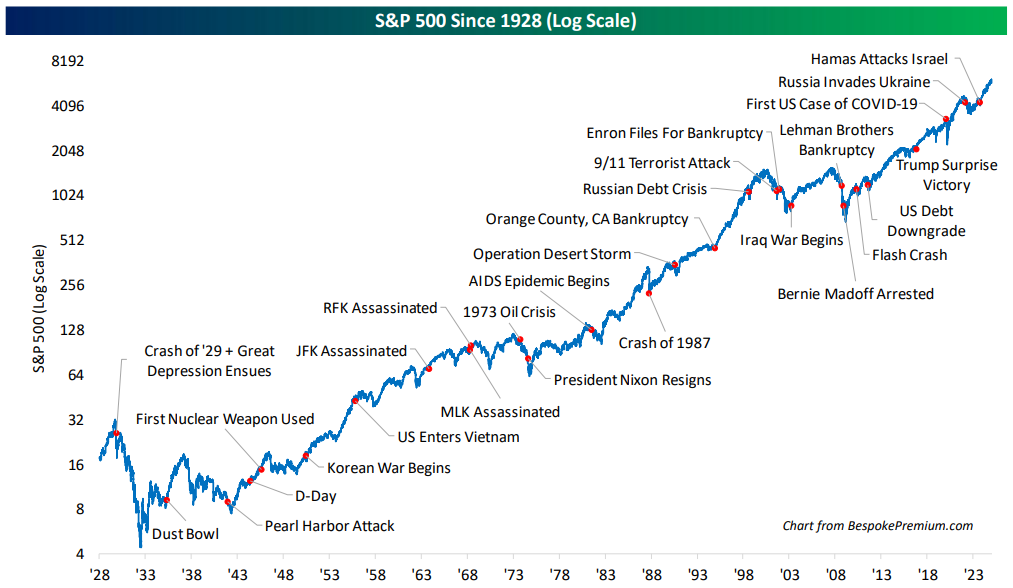

Throughout wars, assassinations, bankruptcies, and market crashes, the U.S. stock market has consistently rebounded to reach new highs. The very long-term log scale chart of the S&P 500 since 1928 below highlights many major events that have affected markets in the short- to intermediate-term along the way to where we are today.

Source: Bespoke Investment Group

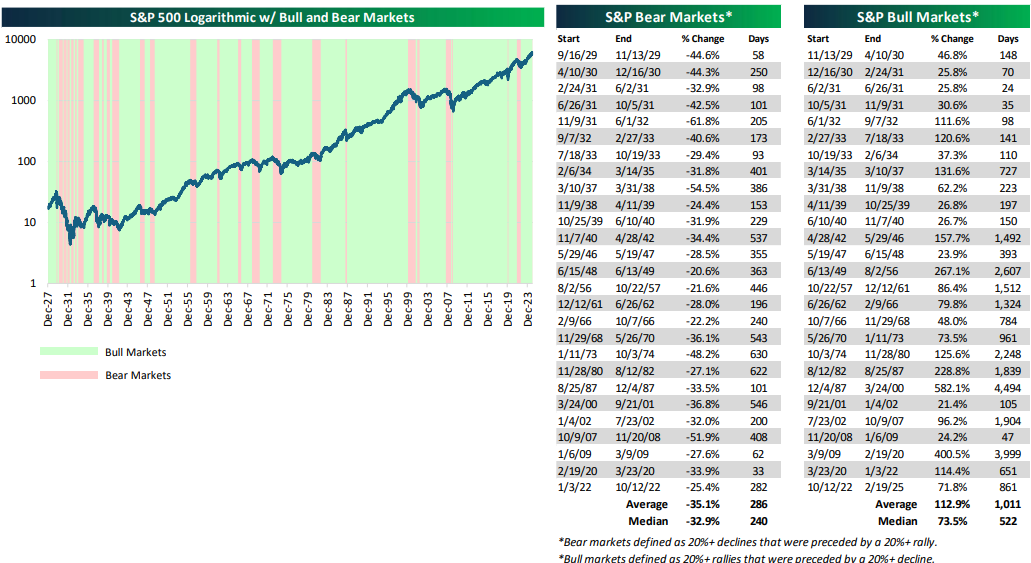

Over this 100-year stretch, the S&P 500 has been in a bull market approximately 78% of the time. Historically, the average bull market for U.S. stocks has endured nearly four times as long as the average bear market. Therefore, if you plan to remain invested for more than a year, bear markets should not be a significant concern. The following chart and tables show historical bull and bear markets in the S&P 500, and the length and percentage change of each market period.

Source: Bespoke Investment Group

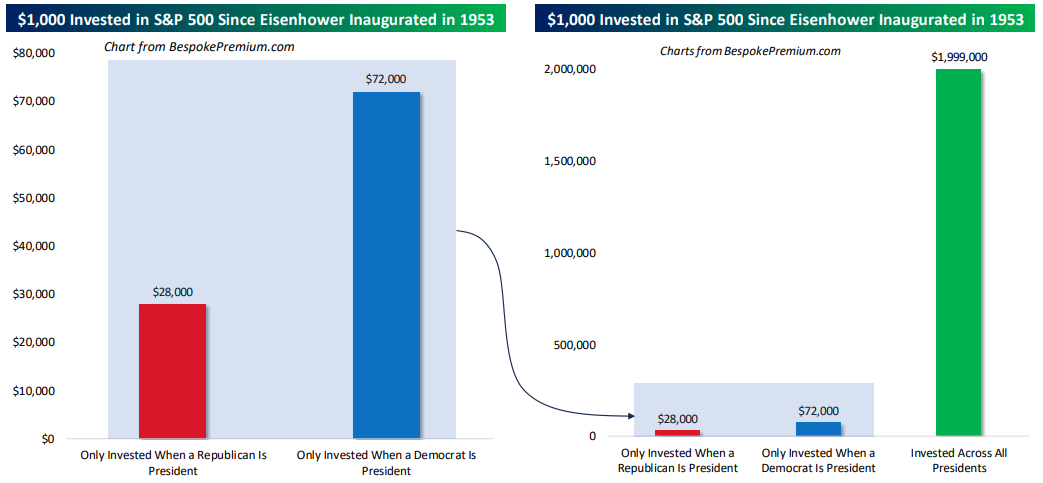

Allowing political beliefs to influence a longer-term "buy and hold" strategy has proven extremely costly for investors. Over the past 70 years, a $1,000 investment in the U.S. stock market (S&P 500) only during Republican presidencies would be worth approximately $28,000 today. In contrast, the same investment held only during Democratic presidencies would be worth more than double that amount, at over $72,000. However, for those who set aside politics and remained invested regardless of the administration in Washington D.C., that initial $1,000 would be worth nearly $2 million today. Again, the charts below highlight that although certain administrations may have a short-term effect on markets, ignoring politics and staying invested provides the best opportunity for long-term success with much stronger returns.

Source: Bespoke Investment Group

Sources: Sources: yahoo finance, Financial Post, First Trust, Bloomberg, Fox Business, Connected Wealth – Richardson Wealth, Canaccord Genuity, Bespoke Investment Group

©2025 Milestone Wealth Management Ltd. All rights reserved.

DISCLAIMER: Investing in equities is not guaranteed, values change frequently, and past performance is not necessarily an indicator of future performance. Investors cannot invest directly in an index. Index returns do not reflect any fees, expenses, or sales charges. Opinions and estimates are written as of the date of this report and may change without notice. Any commentaries, reports or other content are provided for your information only and are not considered investment advice. Readers should not act on this information without first consulting Milestone, their investment advisor, tax advisor, financial planner or lawyer. This communication is intended for Canadian residents only and does not constitute as an offer or solicitation by anyone in any jurisdiction in which such an offer is not allowed.