Market Insights: U.S. Regional Banking Failures

Milestone Wealth Management Ltd. - Mar 17, 2023

Macroeconomic and Market Developments:

- North American markets were mixed this week. In Canada, the S&P/TSX Composite Index was down 1.96%. In the U.S., the Dow Jones Industrial Average decline 0.15% and the S&P 500 Index rose 1.43%.

- The Canadian dollar rallied slightly this week, closing at 72.83 cents vs 72.30 last Friday.

- Oil prices fell this week. U.S. West Texas crude closed at US$66.74 vs US$76.63 last Friday, and the Western Canadian Select price closed at US$50.28 vs US$60.20 last Friday.

- The gold price increased this week, closing at US$1,989 vs US$1,868 last Friday.

- US Inflation increased by 0.4% in February, in line with expectations and currently sits at 6% year over year mainly due to a drop in energy prices.

- The Producer Price Index (PPI) in the U.S. unexpectedly declined by 0.1% in February compared to an expected increase of 0.3%. The PPI currently sits at 4.6% year over year which is welcome news, as it signals easing pressures.

- US Bank News:

- The Silicon Valley Bank (SVB) failure last week sent shock waves through the international banking sector. The US government announced that it will cover all deposits above the FDIC covered amounts.

- First Republic Bank (FRC) was under pressure this week due to fallout from the Silicon Valley Bank failure. The bank was provided with a US$30 billion loan from 11 other banks to instill confidence. As of market close, FRC was trading down 32.80% today.

- Credit Suisse (CSGN) was also affected as a result of the SVB failure, compounded by issues that the bank has been facing for years. As of market close, CSGN was trading down 8.01% today and down 35.86% YTD.

- Meta Platforms Inc. (META) announced plans to cut its workforce by an additional 10,000 workers in the latest round of layoffs. This latest announce brings the total layoffs in the tech sector to date to approx. 95,000.

- Canadian manufacturing sales rose 4.1% in January powered by rise in motor vehicles, petroleum, and coal production marking the strongest rise in manufacturing since February last year.

- CP Rail (CP) won approval from the US Surface Transportation Board for the US$27 billion acquisition of Kansas City Southern. The sale happened in December 2021 but could not be completed until the regulatory approval was granted on March 15th.

Weekly Diversion:

Check out this video: Bernese Mtn Dog Puppy Says Good Morning

Charts of the Week:

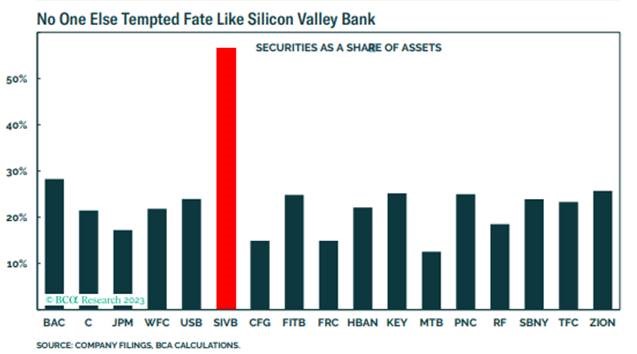

This week’s financial news has been dominated by the banking sector in the U.S., and to a lesser extent internationally, as the markets continue to reel from the Silicon Valley Bank (SIVB) failure. Regional banks in the U.S. have been under some duress with First Republic Bank being the most recent impacted. The market cap of the S&P 1500’s Bank group, the STOXX 600’s banks, and banks in the Bloomberg Asia Pacific Index have dropped 11.4% from March 6th to March 15th. This news sounds grim, however, when we look at the underlying causes for why SIVB failed, we can see that this was not an industry-wide problem, but more due to the management of a few specific banks. As we can see in the chart below, SIVB had a significantly higher level of securities as a percentage of assets, and the type of securities were particularly susceptible to rising interest rates.

Source: BCA Research Inc.

Last weekend, the potential contagion from SIVB was halted by the U.S. government when regulators stepped in to backstop all uninsured capital of SIVB and Signature Banks ensuring that all depositors will have access to all their funds. In addition, the Federal Reserve will be providing a separate facility that will provide loans up to one year for institutions affected by the bank failures. This has been a positive for markets, showing that they took decisive action to protect the U.S. economy by strengthening confidence in their banking system.

Canadian banks have not been immune to recent volatility experienced this week, but they are drastically better positioned due to the stricter regulations in place on capitalization and leverage requirements, and we do not have any concerns on that front presently. In fact, Canada’s banking regulator, the Office of the Superintendent of Financial Institutions (OSFI) required Canadian banks to increase capital requirements on Feb. 1st from 2.5% to 3% to give the financial system more power to protect itself from elevated risks such as this. More importantly, however, Canadian banks were sitting on approximately C$73.3 billion in extra Common Equity Tier 1 capital beyond the regulated minimum as of December 2022 as can been seen in the chart below. The Canadian banking system is considered to be one of the most secure in the world due to this type of oversight.

Source: Office of the Superintendent of Financial Institutions (OSFI)

DISCLAIMER: Investing in equities is not guaranteed, values change frequently, and past performance is not necessarily an indicator of future performance. Investors cannot invest directly in an index. Index returns do not reflect any fees, expenses, or sales charges.

Sources: CNBC.com, Globe and Mail, Financial Post, Connected Wealth, BNN Bloomberg, Tony Dwyer, Canaccord Genuity, First Trust, Seeking Alpha, BCA Research Inc, Office of the Superintendent of Financial Institutions (OSFI)