Market Insights: Intriguing Breadth

Milestone Wealth Management Ltd. - Nov 26, 2022

Macroeconomic and Market Developments:

- North American markets were positive this week. In Canada, the S&P/TSX Composite Index was up 2.02%. In the U.S., the Dow Jones Industrial Average climbed 1.78% and the S&P 500 Index rose by 1.53%.

- The Canadian dollar advanced slightly this week, closing at 74.74 cents vs 74.72 cents last Friday.

- Oil prices declined this week. U.S. West Texas crude closed at US$76.28 vs US$80.13, and the Western Canadian Select price closed at US$50.75 vs US$53.19 last Friday.

- The gold price increased moderately this week, closing at US$1,754 vs US$1,749 last week.

- The release of the minutes from the U.S. Federal Reserve’s last meeting seemed to pacify the markets this week. “A substantial majority of participants judged that a slowing in the pace of increase would likely soon be appropriate,” the minutes stated, giving a bit of hope that this rate hike cycle may end sooner than expected.

- The Bank of Canada’s Tiff Macklem testified before the House Finance Committee where he said inflation remains too strong and higher interest rates are needed. The governor reiterated the central bank expects inflation to stay high for the rest of the year, and to start declining next year. Elsewhere, former Bank of Canada governor Stephen Poloz said that the full effects of interest rate hikes have yet to be felt and will be "even more powerful" than many anticipate.

- Home Capital Group (HCG) announced it has entered into an agreement to be acquired by a wholly-owned subsidiary of Smith Financial Corporation for $44.00/share in cash. Smith Financial is a company controlled by Canadian billionaire Stephen Smith who co-founded First National Financial Corp in 1988, which is a mortgage lender and mortgage-backed securities investor.

- Walt Disney (DIS) surprised investors by brining back Bob Iger as CEO after the surprise exit of CEO Bob Chapek. Iger will serve as Disney's CEO for two years, "with a mandate from the board to set the strategic direction for renewed growth and to work closely with the board in developing a successor to lead the company at the completion of his term". Iger was the CEO for 15 years, from 2005 to 2020, at which time he became chairman of the board of directors, a position he had retired from just 11 months ago.

- Retail Sales in Canada decreased 0.5% in September to $61.1 billion, in line with economists’ expectations. Sales declined in seven of the 11 subsectors, representing 74.9% of retail trade. Statistics Canada also added that the estimate for October Wholesale Sales rose 1.3%.

Weekly Diversion:

Check out this video: This Hawaiian Cat Loves Surfing With His Parents

Charts of the Week:

It has been a nice run of late for equities since their depressed October 12th lows, with the S&P/TSX Composite rising just under 12% and the S&P 500 (in Cdn$) up over 9%. However, the big winner during this period was the international markets (Europe, Asia, Far East), currently up about 15% since then. In addition, the Canadian Bond Universe Index has also enjoyed a nice pop from extremely oversold levels, with long-term interest rates curtailing a bit lately, resulting from Federal Reserve members dialing back their terminal interest rate projections. With any bear market, however, there are oversold bounces within a continued downtrend, and then there are those that end the cycle. We are hopeful for the latter of course, but we have seen an important measure of breadth improve this week, which is very intriguing.

As of Tuesday, 87.7% of the stocks in the S&P 500 are now above their shorter-term 50-day moving averages (DMA) while 60% are above their longer-term 200-DMAs. The shorter-term breadth is very strong of late but still not quite above the August highs. However, it is strength in the longer-term breadth that bulls prefer to see, and that is just what the doctor ordered this week with long-term breadth now stronger than the August highs. As the following chart illustrates, you can see the orange line, which represents the percentage of S&P 500 stocks above their respective 200-DMAs, break-out to new highs. This is a very encouraging sign that this could possibly be more than just a short-term oversold rally, and perhaps the start of a longer-term uptrend.

Source: Bespoke Investment Group

What is interesting is that breadth weakened in the months leading up to the last peak in the markets. You can see the orange line below (long-term breadth) diverging from the blue line (S&P 500 price). Now on the flip side, breadth has rapidly moved up to new highs above August, whereas the S&P 500’s downtrend is still intact and about 7% off from reaching that August high. Breadth usually, but not always, leads price. So again, this is an encouraging signal.

Source: Bespoke Investment Group

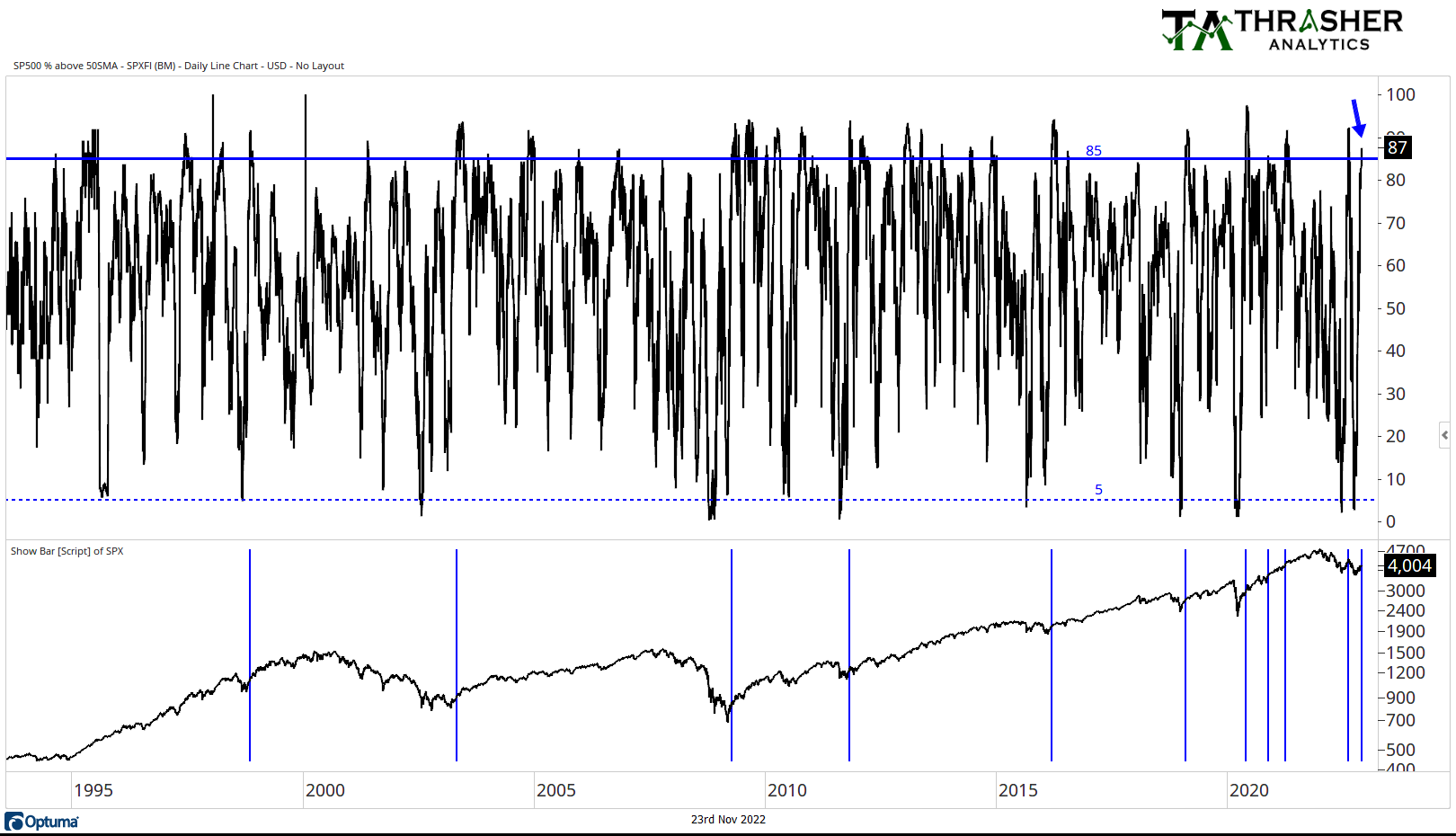

The rapid ascent in the percentage of stocks above their shorter-term 50-DMAs has also been a positive. We have seen the percentage rise from a recent low of 3% all the way up to 87% in less than two months. A rise in short-term breadth from below 5% to above 85% has historically been a very bullish development, and an accurate one at that. As you can see below, the blue vertical lines show the past 11 occurrences of this signal going back to the early 90s. What is important to note is that this signal has been very accurate in denoting either the start or continuation of a bull phase for markets. If you look at the large price declines for the S&P 500 in the table below, the blue line positive signal has almost always occurred after the bottom was realized. Over the past thirty years, the track record for this signal has been virtually fool-proof until just recently, when it was triggered in August, but markets resumed their downward trend into October. We now have this signal triggering again, so we are hopeful that August was a rare false positive, and that this line will in hindsight be a point in time that occurs after a true longer-term low.

Source: @AndrewThrasher, Thrasher Analytics, Optuma

DISCLAIMER: Investing in equities is not guaranteed, values change frequently, and past performance is not necessarily an indicator of future performance. Investors cannot invest directly in an index. Index returns do not reflect any fees, expenses, or sales charges.

Sources: CNBC.com, Globe and Mail, Financial Post, Connected Wealth, BNN Bloomberg, Tony Dwyer, Canaccord Genuity, First Trust, Bespoke Investment Group, Thrasher Analytics, Optuma