Market Insights: Markets Rejoice on Peak Inflation

Milestone Wealth Management Ltd. - Nov 12, 2022

Macroeconomic and Market Developments:

- North American markets were up significantly this week. In Canada, the S&P/TSX Composite Index increased 3.40%. In the U.S., the Dow Jones Industrial Average rose 4.15% and the S&P 500 Index advanced 5.90%.

- The Canadian dollar was positive this week, closing at 75.43 cents vs 74.18 cents last Friday.

- Oil prices were down this week. U.S. West Texas crude closed at US$88.96 vs US$92.47, and the Western Canadian Select price closed at US$59.59 vs US$63.63 last Friday.

- The gold price finished significantly higher this week, closing at US$1,767 vs US$1,681 last week.

- The “Red Wave” that was expected on Tuesday did not come to fruition with control of the House and the Senate still undecided. Ballots are still being counted but the expectation that the Republican Party would seize a significant number of seats was overstated in early polls. Regardless of the results, Biden and the Democratic Party are treating this outcome as a major victory.

- The US CPI (Consumer Price Index) increased by 0.4% in October vs. an expected increase of 0.6%. The CPI news came as a welcome relief for markets as a potential signal of cooling inflation and resulted in a massive rally on Thursday. More information can be found in the Charts section below.

- Cryptocurrencies took a massive hit this week with the massive sell-off of FTX’s owned crypto token due to leverage and liquidity concerns, resulting in the company declaring bankruptcy on Friday. The news rocked the Crypto Market as the failure of the popular exchange demonstrated the lack of regulation in the industry. At market close on Friday, Bitcoin was trading under US$17,000 and Ethereum was trading under US$1,300.

- Facebook parent Meta (META) announced the company would lay off 13% of their workforce in a response to the massive downturn this year, which was the result of the company’s excessive spending and investment in the “metaverse”. Markets reacted positively to the news with the share price up 20.86% for the week.

- Disney (DIS) reported lower profit and revenue compared to analyst expectations with key segments underperforming. The share price fell 6.01% for the week on the negative revenue news and fear that streaming growth could taper off.

- Canada Pension Plan Investment Board saw net assets grow to $529 billion in its second quarter, up from $523 billion last quarter. The increase represents a gain of 0.2% and an outperformance of global indices. To date, the fund has posted 5-Yr Returns of 9.5% and 10-Yr Returns of 10.1%.

- Canadian Tire Corporation Inc. (CTC.A) reported lower earnings per share (EPS) than expected at $3.34 EPS vs. $3.92 EPS. The company’s retail segment was the main drag on earnings due to rising freight and product costs. Despite the results, the company elected to increase the annual dividend to $6.90/share.

- Here is a link to a short video from Canaccord’s chief U.S. Strategist Tony Dwyer entitled The Temporary Sweet Spot and Year-End Rally DWYER VLOG

Weekly Diversion: Relaxing

Charts of the Week:

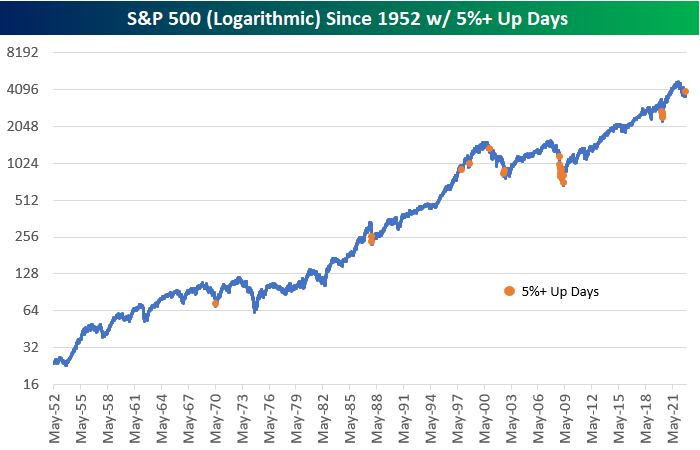

A Look at 5%+ Up Days:

On Thursday, the S&P 500 gained 5.54%; the 15th-best trading day since 1953, when the current 5-day trading week began. The table below shows historical performance of trading days with 5%+ increases since 1953. Although welcome news, historically the S&P 500 has declined on average 0.77% the next day and fallen 1.73% the following week. This is often seen as a small correction to a massive rally. In contrast, however, the index has averaged a 10.37% increase over the next 6 months and averaged 27.95% over the next year with positive returns occurring 20 out of 22 times. This forward 1-year average return of 28% is more than two and a half times larger than normal for all periods. At market close today, the S&P 500 closed 0.92% higher.

Source: Bespoke Investment Group

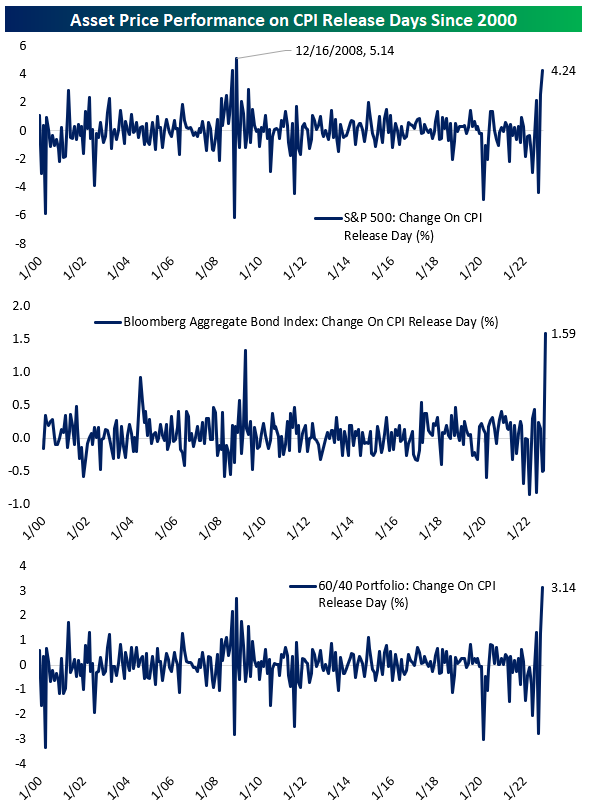

Markets Rejoice on Peak Inflation:

U.S. Headline and Core CPI numbers on Thursday came in below analyst expectations led by lower medical care costs, lower rent growth, a drop in average used vehicle prices, and lower costs for durables. As of yesterday, when the chart was generated, stocks were up 4.2% and closed up 5.54%, beating the previous highest single CPI rally increase since 2000 (2008 at 5.1%). Also, bond prices saw a rally yesterday with 2-year yields down 30 bps (largest decline since 2008). Balanced portfolios (60/40 split of equities and fixed income) also saw relief, increasing over 3% based on a hypothetical blended portfolio using the Bloomberg Aggregate Bond Index and the S&P 500.

Source: Bespoke Investment Group

This week’s U.S. CPI news is a good start, but where will the Fed go from here? The chart below shows the actual CPI year-over-year (YoY)% by month and the Fed Funds rate %. The chart also shows future YoY CPI changes month-over-month (MoM) and hypothetical future Fed Fund rates. To get back to the 2% CPI YoY range by the middle of 2023, we would need to see future CPI increases limited to 0.2% MoM based on expected Fed Fund futures. If CPI continues growing at 0.4% MoM, headline CPI would end just under 5% by September 2023, provided this data holds true.

Source: Bespoke Investment Group

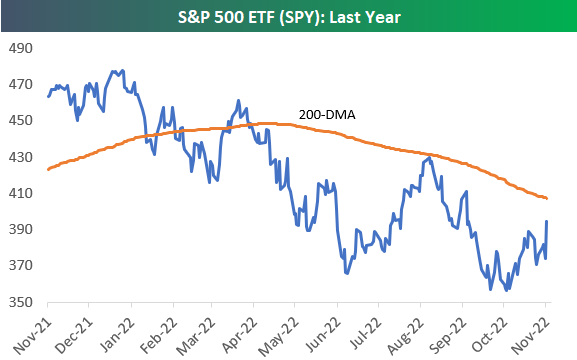

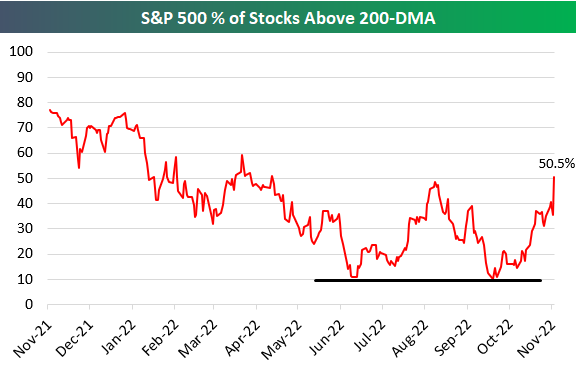

Positive Breadth Around the 200-DMA:

The 200-day moving average (DMA) is used to help filter out noise from single-day or shorter movements by reflecting a longer-term trend. As demonstrated in the chart below, the S&P 500 ETF’s (SPY) 200-DMA has been trending lower for the past 6 months and has not closed above its 200-day average since the downturn began.

Source: Bespoke Investment Group

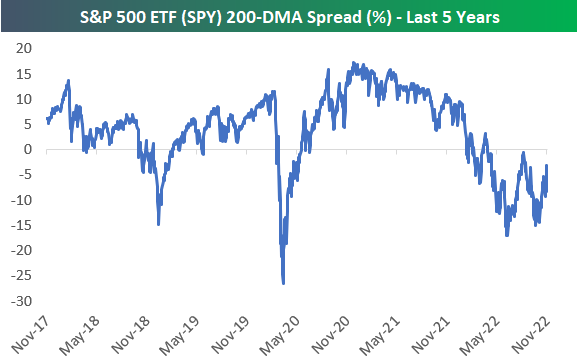

Although the ETF is trading up 10% from its October low, it is still more than 3% below its 200-day moving average.

Source: Bespoke Investment Group

There is room for optimism; with the rally yesterday, we saw over 50% of the companies that make up the S&P 500 close above their own 200-day moving average, as seen in the chart below. While the S&P 500 index as a whole, remains 3% below its 200-DMA, we are starting to see more companies trend in a positive direction. This is an important positive divergence for markets.

Source: Bespoke Investment Group

DISCLAIMER: Investing in equities is not guaranteed, values change frequently, and past performance is not necessarily an indicator of future performance. Investors cannot invest directly in an index. Index returns do not reflect any fees, expenses, or sales charges.

Sources: CNBC.com, Globe and Mail, Financial Post, Connected Wealth, BNN Bloomberg, Tony Dwyer, Canaccord Genuity, First Trust, Bespoke Investment Group