Market Insights: November and Election Cycle Seasonality

Milestone Wealth Management Ltd. - Nov 04, 2022

Macroeconomic and Market Developments:

- North American markets were down this week. In Canada, the S&P/TSX Composite Index declined slightly by 0.11%. In the U.S., the Dow Jones Industrial Average fell 1.40% and the S&P 500 Index dropped 3.35% due to heavy selling in the Tech sector.

- The Canadian dollar was up this week, closing at 74.18 cents vs 73.49 cents last Friday.

- Oil prices were positive this week. U.S. West Texas crude closed at US$92.47 vs US$88.23, and the Western Canadian Select price closed at US$63.63 vs US$58.67 last Friday.

- The gold price finished higher this week, closing at US$1,681 vs US$1,644 last week.

- The markets were focused on the U.S. Federal Reserve meeting this week, with its rate announcement being released on Wednesday. The central bank approved a fourth consecutive 0.75% interest rate increase, to a target range of 3.75% - 4.00%, the highest level since January 2008. The statement signaled a potential change in how it will approach monetary policy to bring down inflation by saying the Fed “will take into account the cumulative tightening of monetary policy, the lags with which monetary policy affects economic activity and inflation, and economic and financial developments.”

- Johnson & Johnson (JNJ) said on Tuesday it would buy heart pump maker Abiomed (ABMD) in a $16.6 billion deal, its biggest in nearly six years. J&J’s $380/share offer represented a 50.7% premium to the last closing price. In addition, Abiomed shareholders will also get rights to receive up to $35/share in cash if certain commercial and clinical milestones are achieved.

- Cenovus Energy (CVE) reported lower than expected Q3 cash flow of $1.49/share vs the expected $1.61/share, with production of 777.9 MBOE/D vs 787.8 MBOE/D expected. The company declared a variable dividend of $0.114/share, which is in addition to the declared $0.105/share dividend in December.

- Canadian Natural Resources (CNQ) reported better than expected Q3 cash flow at $4.60/share vs the $4.42/share forecasted, with earnings of $3.09/share vs the $2.84/share forecasted, and production of 1,338.9 MBOE/D vs the 1,338.1 MBOE/D forecasted. The company announced it will be increasing its quarterly dividend by 13.3% to $0.85/share from $0.75/share.

- The U.S. ISM Non-Manufacturing (Services) Index declined to 54.4 in October, below the expected 55.3 (levels above 50 signal expansion and levels below signal contraction). The major measures of activity moved mostly lower in October, but nearly all stand above 50, signaling slowing growth.

- On Friday, North American employment numbers were released, with both Canada and the U.S. beating expectations. In Canada, the economy added 108,000 jobs compared to the significantly lower forecast of just 10,000. The unemployment rate held steady at 5.2%. The U.S. economy added 261,000 jobs vs the estimated 205,000, although the unemployment rate increased slightly to 3.7% from September’s 29-month low of 3.5%.

- Here is a link to a short video from Canaccord’s chief U.S. Strategist Tony Dwyer entitled Our Plan As Year-End Rally Plays Out: DWYER VLOG

Weekly Diversion:

Charts of the Week:

We have discussed equity investing seasonality many times in our comments over the years. As we have now welcomed November, we wanted to highlight this month as the first of the seasonally strong six months for equities. In addition, we are also about to begin the best period to be invested from the perspective of the four-year U.S. Presidential Cycle.

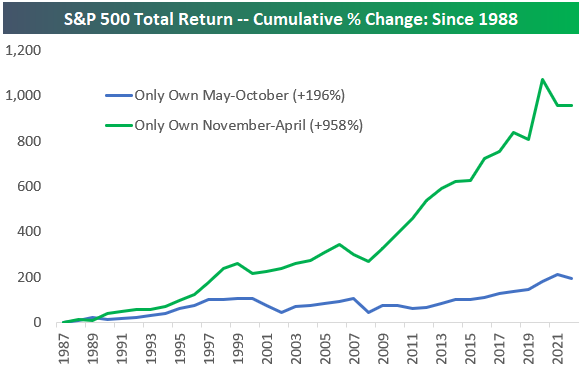

The following chart illustrates well what we mean by the seasonally strong period for equities. As you can see, if one was only invested in the market from the beginning of November to the end of April, their total cumulative return (including dividends) since 1998 would be 958% versus just 196% for the remaining months (May-October) for the same years. These numbers are even more drastic if you go back to 1928, where your cumulative price return (not including dividends) would have been 5,145% vs. 274%. You may be asking yourself “why not implement this strategy?”. The main reason of course is that if you are fully invested the entire period, your return is even larger compared to just owning from November to April. In addition, this pattern doesn’t hold true every year, but does hold true for a majority. For example, the S&P 500 dropped significantly the last two months of 2018, and we all remember the first quarter of 2020, especially March, where the S&P 500 was down at one point 35% peak to trough over just a four-week period from late February to late March. The total return for the S&P 500 from November 1, 2019, to April 30, 2020 ended up being -3.1% (only thanks to a sharp recovery in April). However, the total return during the seasonally weak period of May 1, 2020, to October 31, 2020, was 13.3%. It would have been very detrimental to not stay invested over this year. As we stand today however, equity seasonality still provides a potential tailwind from now until April.

Source: Bespoke Investment Group

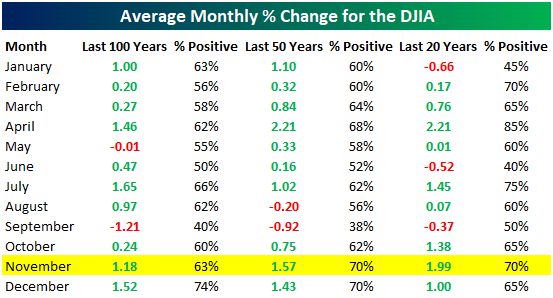

Looking at November specifically, here is a table that shows how the U.S. Dow Jones Industrial Average has performed each month of the year, going back various periods over the last 100 years. We have highlighted November, which has been the second-best month in the last 20 and 50 years, only behind April. The positive percent rate at 70% is the strongest in the last 50 years (along with December) and the third best over the last 20 years.

Source: Bespoke Investment Group

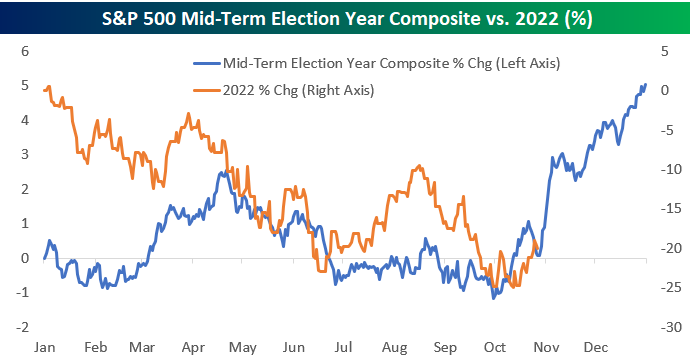

Moving on to the U.S. Presidential Cycle, November 8th marks the US Mid-Term Election date. According to political polls from FiveThirtyEight.com, it appears the Republicans will regain control of Congress. Based on history, regardless of who has control of Congress, the third year of the four-year election cycle has been by far the strongest for equities, and even more so for the 6-month period (which is in line with the equity seasonality factor above) right after the Mid-Terms. The second year of the cycle, which it is right now in 2022, has historically been the worst. Where do we stand this year versus past second years of the cycle? As you will see below, the current year is in orange, and the blue line is all second years dating back to 1928. It has been a very difficult one so far this year, but there is hope looking at the historical blue line for the last two months of the year.

Source: Bespoke Investment Group

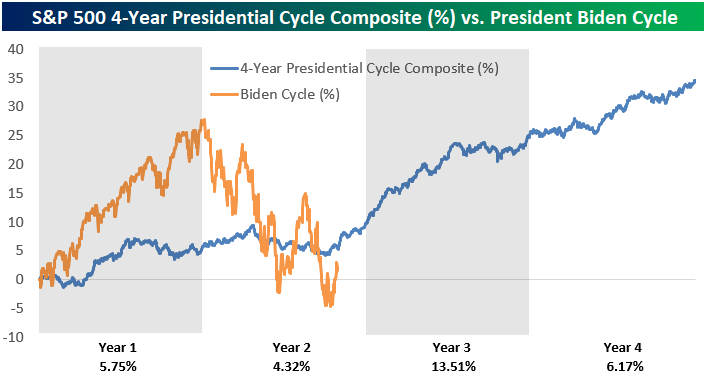

Here is a composite chart for the S&P 500 throughout the U.S. Presidential Cycle (blue line) with the current cycle (orange line) of Biden’s time overlaid. You will note the average price return of those calendar years at the bottom of the chart. While the magnitude of the up and down movements of the past two years has been much larger than the average of the past, the pattern could still hold true. If there was ever a time for a tailwind of both equity seasonality and the U.S. Presidential cycle, especially the next six months, now may be that time.

Source: Bespoke Investment Group

DISCLAIMER: Investing in equities is not guaranteed, values change frequently, and past performance is not necessarily an indicator of future performance. Investors cannot invest directly in an index. Index returns do not reflect any fees, expenses, or sales charges.

Sources: CNBC.com, Globe and Mail, Financial Post, Connected Wealth, BNN Bloomberg, Tony Dwyer, Canaccord Genuity, First Trust, Bespoke Investment Group, FiveThirtyEight.com