Market Insights: Costs of Hedging Equity Risk Goes Through the Roof

Milestone Wealth Management Ltd. - Sep 23, 2022

Macroeconomic and Market Developments:

- North American markets were down significantly this week. In Canada, the S&P/TSX Composite Index was down 4.53%. In the U.S., the Dow Jones Industrial Average declined 4.00% and the S&P 500 Index was dropped 4.65%.

- The Canadian dollar dropped again this week, due to the relentless strength of the U.S. dollar this year, closing at 73.56 cents vs 75.36 cents last Friday.

- Oil prices were down this week. U.S. West Texas crude closed at US$79.31 vs US$85.28, and the Western Canadian Select price closed at US$56.79 vs US$63.94 last Friday.

- The gold price also declined this week, closing at US$1,644 vs US$1,675 last week.

- The story of the week was the U.S. Federal Reserve meeting that wrapped up on Wednesday. The central bank raised benchmark interest rates by 0.75% for the third consecutive time, to a range of 3.00% - 3.25%, the highest it has been since early 2008. The market was largely expecting this move, however the Fed did come off much more hawkish in their comments and as such, the U.S. stock market finished down roughly 1.7% on Wednesday and continued lower throughout the remainder of the week.

- Another big driver of global markets was an announcement on Friday by the new U.K. Prime Minister Liz Truss, revealing a new plan to stimulate the economy with tax cuts and investment incentives. With economists predicting that these measures will exacerbate inflation that is already around 10% in the country, interest rates jumped dramatically on the news, pushing down the price of bonds and crushing the British Pound to a level not seen since 1985.

- Agnico Eagle Mines (AEM) and Teck Resources (TECK.b) jointly announced that Agnico Eagle has agreed to purchase a 50% interest in Minas de San Nicolás, a wholly-owned subsidiary of Teck which owns the San Nicolás copper-zinc development project located in Zacatecas, Mexico.

- Canadian inflation data was released this week. The Consumer Price Index (CPI) rose 7.0% on a year-over-year basis in August, down from a 7.6% annual gain in July. Excluding the volatile price of gasoline, prices rose 6.3% year-over-year in August, following a 6.6% increase in July.

- The Teranet–National Bank housing price index, which measures 11 Canadian metropolitan areas, fell 2.4% from July to August, with nine of the cites falling. The largest declines were recorded in Hamilton (-5.4%), Ottawa-Gatineau (-3.8%), Halifax (-3.6%) and Toronto (-3.5%). Calgary and Edmonton bucked the trend with month-over-month gains of 1.3% and 2.8% respectively.

- Statistics Canada announced that Canadian Retail Sales fell 2.5% to $61.3 billion in July, the first drop in seven months as sales at gasoline stations and clothing stores decreased. However, the agency says its initial estimate for August pointed to a gain of 0.4% for the month.

Weekly Diversion:

Check out this video if you want to learn how to fish for chipmunks.

Charts of the Week:

In looking for signs of excessive pessimism and angst that can provide a contrarian upside signal, look no further than the S&P 500’s put/call premium, which has recently spiked higher than 2002, 2008, 2016 and 2020. Put and call options are leveraged contracts tied to an underlying stock or index, that are primarily used by institutional and options traders to either speculate up or down, to provide income, or to hedge a position or portfolio. You pay a premium for the put or call contract, giving you the right to sell or buy the stock/index, respectively, at a specific price within a specific time frame. The more in demand a put or call is, the higher the premiums rise. Right now, the cost to protect/insure a portfolio with a put option has never been higher. As you can see in the following chart, the put/call premium on the S&P 500 has spiked off the charts to a level never seen in 20 years. In the past, any level well above 1.5 has been at or close to a very long-term bottom. In 2002, 2016 and 2020 it was very close to the bottom, and in 2008, the signal occurred just a few months (last leg down) prior to the bottom that ultimately started the current secular bull market that we remain in.

Source: Game of Trades

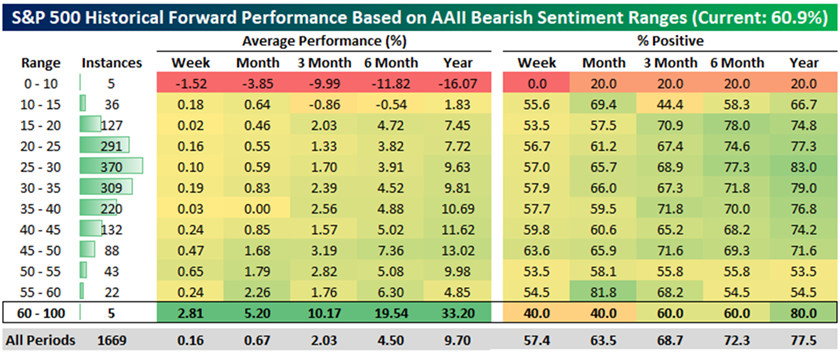

As one can imagine, the recent equity pullback off the summer highs is pushing investor sentiment back to extreme levels. In fact, the American Association of Individual Investors (AAII), a widely followed weekly sentiment survey, is now reporting a bearish sentiment level above 60%, a new high for this cycle. A level above 60% has only occurred a couple of other times going all the way back to start of the survey in July 1987. Just a few readings in 1990 and 2008/9 topped the current bearish sentiment reading of 60.9%. A weekly survey level over 60% has occurred only five times out of 1,669 trading weeks. As painful as markets have been this year, a reading over 60% has resulted in by far the best, if not spectacular, forward-looking returns over the next year (see highlighted line in the table below), almost four times the average return for all periods and with a positive return rate of 80%. While a reading over 60% certainly doesn’t necessarily mean stocks have made their lows, it does suggest forward returns are very good even assuming we make a fresh new low for the market.

Source: Bespoke Investment Group

Being as this year is a mid-term U.S. election year, which hasn’t typically been the equity market’s better periods, we thought it would be useful to compare 2022 to other correlated mid-term years where the market was struggling. The S&P 500 is officially down 20% year-to-date as of September; 2022 now joins 1962, 1974, 2001, 2002, and 2008 as the only years to ever do that since 1950. Only 2008 saw things get worse by the end of the year though and only 1962 avoided a recession. We do not believe 2008 is a good comparison to today’s environment. However, 1962 could provide a relatively decent blueprint (beige line below) as it currently looks a lot like 2022 at this point. Other similarities are a new Democratic President, a mid-term year, supply chain issues, Cuban missile crisis, etc. In that year, the S&P 500 didn’t bottom until October 23rd, but then rallied 19% into the end of the year.

Sources: Ryan Detrick & Carson Group LLC

The last chart we wanted to show this week is from the Bank of America Global Fund Manager Survey. The latest survey shows that allocations to European equities dropped to a record low. Europe is basically the epicenter of the 2022 macro decline and recession warnings, so we should probably expect to see this. Perhaps we can call it rational fear. However, at some point it will certainly become irrational, and thus a good long-term opportunity. In our Milestone core and ETF mandates, we exited all of our international equity much earlier in the year and we currently remain out of those markets.

Sources: Callum Thomas, Topdown Charts

DISCLAIMER: Investing in equities is not guaranteed, values change frequently, and past performance is not necessarily an indicator of future performance. Investors cannot invest directly in an index. Index returns do not reflect any fees, expenses, or sales charges.

Sources: CNBC.com, Globe and Mail, Financial Post, Connected Wealth, BNN Bloomberg, Tony Dwyer, Canaccord Genuity, First Trust, Bespoke Investment Group, Game of Trades, Carson Group LLC, Bank of America, Datastream, American Association of Individual Investors, Topdown Charts