Market Insights: The Streak Finally Ends

Milestone Wealth Management Ltd. - Jul 22, 2022

Macroeconomic and Market Developments:

- North American markets were positive this week. In Canada, the S&P/TSX Composite Index was up 3.17%, recouping most of last week’s drop. In the U.S., the Dow Jones Industrial Average increased 1.95% and the S&P 500 Index was up 2.55% this week.

- The Canadian dollar was positive this week, closing at 77.45 cents vs 76.72 cents last Friday.

- Oil prices were down again this week. U.S. West Texas crude closed at $94.66 vs $97.49 USD last Friday, and the Western Canadian Select price closed at $74.16 vs $76.42 last Friday.

- The gold price recovered somewhat this week, closing at $1,724 vs $1,703 USD last Friday.

- Canadian engineering company IBI Group (IBG) has reached a takeover agreement with Amsterdam-listed design and consultancy firm Arcadis (ARCAD.NA) whereby Arcadis will acquire all issued and outstanding shares of IBI Group for $19.50/share. The transaction price represents a premium of 30% to the previous closing price and is expected to be completed in second half of 2022.

- Suncor Energy (SU) announced this week that it has entered into an agreement with activist investor Elliott Investment Management, in which Suncor's board will appoint three new independent directors, two of whom will serve on the search committee for a new CEO. The board will also form a new committee to oversee a strategic review of Suncor's PetroCanada division.

- West Fraser Timber (WFG) has been approached by private equity firm CVC Capital and manufacturer Kronospan with a joint takeover offer for West Fraser. The companies have informed management of their intention to proceed with negotiations however financial details have yet to be announced.

- Inflation data in Canada was released on Wednesday morning. The Consumer Price Index (CPI) increased 0.6% for the month of June vs expectations for a 0.9% increase. The CPI is up 8.1% from one year ago, slightly lower than the expected 8.4%, but still represents an increase in inflation from 7.7% from May 2021 to May 2022.

- Netflix (NFLX) surprised with more upbeat earnings this week. The streaming service only lost 970,000 subscribers, which was better than feared. The overall loss of 1.2 million subscribers over the year is a significant pendulum swing from the 26 million added during the first half of 2020. Despite the contraction, Netflix reported $1.4 billion in earnings, up 6% year over year, and an increase in revenue of 9%.

- Here is a link to a short video from Canaccord’s chief U.S. Strategist Tony Dwyer entitled The Fantastic Four Recession Indicators: DWYER VLOG

Weekly Diversion:

Check out this video of a scuba diver getting photobombed by a shark.

Charts of the Week:

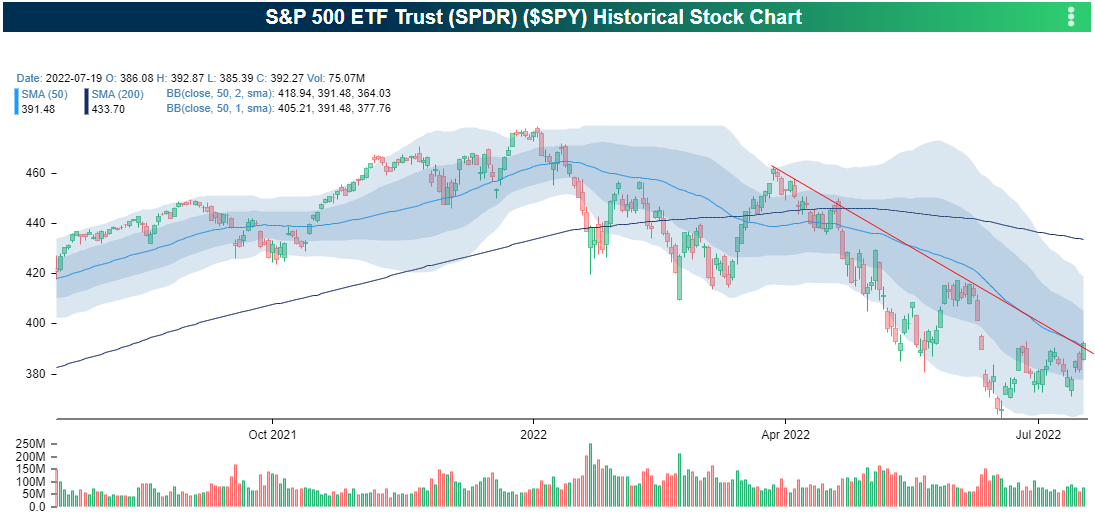

The tone to markets this week was an improvement from last week, especially for the S&P/TSX Composite. The title “The Streak Finally Ends” is referring to the streak of the S&P 500 Index trading below its 50-day moving average (DMA). This week, the U.S. large cap market finally managed to trade and close above its 50-DMA, ending a streak of 60 consecutive trading days. As the chart below shows, it also appears to have closed above the downtrend line created from the March high. While this by no means ensures the low is in, it is an encouraging sign that June may be a low. Since the middle of June, we have been saying there is a strong set up for a potential short-term summertime rally that could at least recover some of the recent pullback. However, a longer period of time of market support above the pre-COVID high, a declining headline inflation number in the second half of this year and a change in tone from the Federal Reserve later this year in terms of tightening financial conditions, is likely needed to ensure the low is in.

Source: Bespoke Investment Group

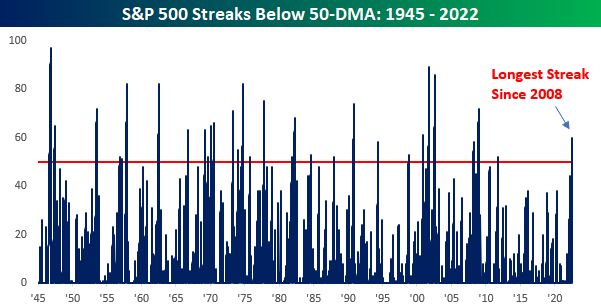

If you are wondering if the streak of 60 consecutive trading days below the 50-DMA is a long time historically for the S&P 500, it certainly is. In fact, since WWII, this is the longest streak since December 2008 (about two months before the market’s ultimate bottom), and the 31st streak of 50 or more trading days.

Source: Bespoke Investment Group

While it is encouraging that this negative trend has ended, we think that the accompanying signal of the S&P 500 ending the streak with a rally of greater than 2% is one worth noting. The following table shows the historical performance of the S&P 500 after the end of these 50+ day streaks below the 50-DMA. The light blue bar shows how it has performed after the streak ends and the dark blue line is all periods. As you can see, while very short-term performance has been better than average, it has not been an overly positive sign over the next 3- and 6-month periods, but importantly it has been a strong sign of outperformance over the following year. However, of the 30 prior occurrences, there have been only 10 where the streak ended on a day with the S&P 500 surging more than 2%, like it did on Tuesday. This is shown by the grey bar below. This paints a much different picture, showing that when this has occurred, the forward-looking performance has been extremely strong, with median outperformance over every time period. Over the next 6- and 12-months, the S&P 500 has returned more than double the median return for all periods. Also worth mentioning, the one-year return has been positive in 100% of the occurrences of streaks ending with a 2%+ rally. While this is not indicative of future results today, we hope this signal stays true this time around.

Source: Bespoke Investment Group

Sources: CNBC.com, Globe and Mail, Financial Post, Connected Wealth, BNN Bloomberg, Tony Dwyer, Canaccord Genuity, First Trust, Bespoke Investment Group