Market Insights - U.S. Mega-caps Starting to Weigh Down the Market

Milestone Wealth Management Ltd. - Apr 22, 2022

Macroeconomic and Market Developments:

- North American markets were down again this week. In Canada, the S&P/TSX Composite Index fell 3.06%. In the U.S., the Dow Jones Industrial Average declined 1.86% and the S&P 500 Index was down 2.75%.

- The Canadian dollar was also down this week, closing at 78.66 cents vs 79.31 cents last Friday.

- Oil prices were lower this week. U.S. West Texas crude closed at $101.16 vs $106.95 last Friday, and the Western Canadian Select price closed at $89.18 vs $93.96 last Friday.

- The gold price also closed down this week, closing at $1,933 vs $1,974 last Friday.

- Canada’s Consumer Price Index (CPI) for March came out this week, showing the inflation rate at 6.7% over the past year. This level is up from February's 5.7% reading and was well above the forecasted 6.1%. Core CPI (excluding food and energy) came in at 2.8% compared to 2.7% estimated.

- Canadian retail sales increased by 0.1% in February, above expectations for a modest drop following January's 3.2% gain. Statistics Canada’s early estimate points to retail sales being up another 1.4% in March.

- U.S. private equity firm Blackstone announced that it is buying American Campus Communities (ACC) for $12.8 billion including debt, in a deal at $65.47/share, nearly 14% higher than ACC’s last stock close. The student housing company owns 166 properties across 71 university markets including Arizona State University and the University of Texas at Austin.

- Netflix (NFLX) on Tuesday reported a loss of 200,000 subscribers during the first quarter and warned of deepening trouble ahead as the company is forecasting a global paid subscriber loss of 2 million for the second quarter. The last time Netflix lost subscribers was October 2011 when it shed 800,000 paid users. As a result, the stock price was down a whopping 35.12% on Wednesday and by the week’s end is down a total of 64.23% so far in 2022.

- Rogers Communications (RCI.b) reported earnings of $0.91/share, well above the $0.83/share expected, however revenue was slightly lower than expectations at $3.62 billion vs $3.63 billion expected. In addition, indications are looking positive that its proposed takeover of Shaw Communications (SJR.b) will move forward.

- Tesla (TSLA) reported impressive earnings after the market closed on Wednesday. Earnings came in at $3.22/share compared to $2.26/share expected on revenue of $18.76 billion vs $17.80 billion expected. Automotive revenue reached $16.86 billion, up 87% from the same period last year. Tesla’s share price was up 3.23% on Thursday as a result.

- Here is a link to a short video from Canaccord’s chief U.S. Strategist Tony Dwyer entitled Using Patience Can Be Frustrating: DWYER VLOG

Weekly Diversion:

Check out this video of an incredible proposed $5 billion resort on the shores of the Red Sea.

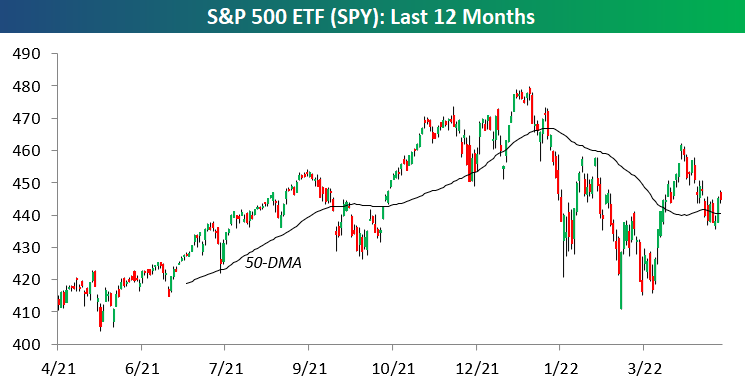

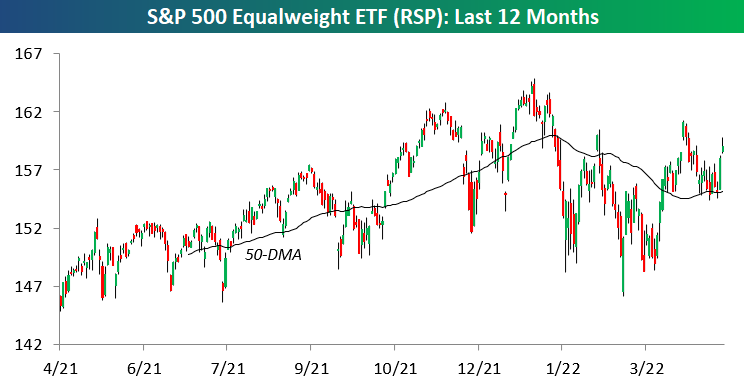

Charts of the Week:

Here are two charts of the S&P 500 Index over the last 12 months from a market-weighted perspective vs equal-weighted. Since 2014, the market-weighted index has propelled the U.S. stock market higher than indicated by the average stock, due to the overpowering technology sector which had been growing at a rapid pace and becoming a large portion of the market-weighted index. However, there has been a reversal in this trend recently, or perhaps better described as a reversion to the mean. Mega-caps can work both ways: either they’re trending higher and helping major indices, or trending lower and holding the major indices back. The latter is the case recently with the S&P 500 Index down about 10% year to date as of today compared to the S&P 500 Equal Weight Index being down about 6%.

Source: Bespoke Investment Group

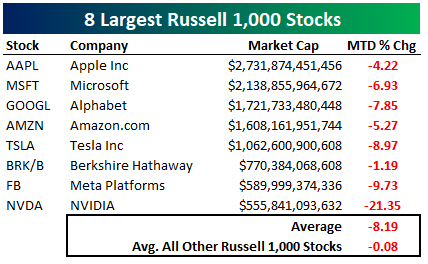

The table below shows the largest eight companies in the U.S. and their month-to-date changes as of Wednesday this week. This average return of -8.2% in April compares to a roughly flat return for all the ~1000 stocks in the Russell 1000 index. This is indicative of a correcting top-heavy market, while the average stock has been in a healthier position lately.

Source: Bespoke Investment Group

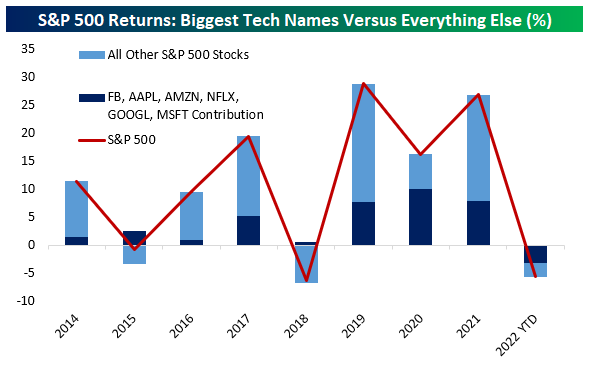

Here is another chart showing just how much these largest companies have impacted U.S. large cap indices. It shows the calendar year returns of the S&P 500 but broken down between seven of the biggest tech names and all other S&P 500 stocks. The year 2020 was a standout where more than half of the entire market’s returns came from just these seven names. They also were hugely behind the big moves of 2019 and 2021. However, this year is the opposite, and they are now attributing about half of the YTD decline.

Source: Bespoke Investment Group

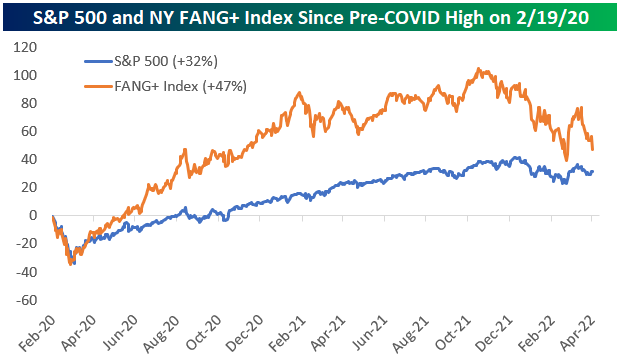

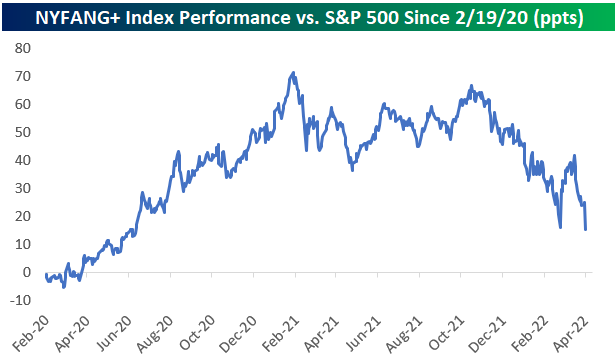

The so called “FANG+” stocks make up seven of these eight largest stocks, with also the addition of Netflix, Alibaba and Baidu. From April 4th to 19th, the FANG+ index is down 17% and is down 28% from its all-time high. The chart below shows these FANG+ stock returns vs the overall S&P 500 since the pre-COVID high of February 2020. This group of stocks peaked out in early 2021 with an incredible outperformance spread of more than 70% compared to the overall market. This outperformance has been rapidly eroding since last November (as per our reversion to the mean comment above) and the spread is now only about 15%. This is putting pressure on U.S. headline equity indices, compared to our low-tech but energy/materials-rich S&P/TSX Composite which is still slightly positive so far in 2022 as of today on a total-return basis.

Source: Bespoke Investment Group

Sources: CNBC.com, Globe and Mail, Financial Post, Connected Wealth, BNN Bloomberg, Tony Dwyer, Canaccord Genuity, First Trust, Bespoke Investment Group