Market Insights: Four Strong Days

Milestone Wealth Management Ltd. - Mar 25, 2022

Macroeconomic and Market Developments:

- North American markets were higher again this week, after a huge relief rally last week in the U.S. In Canada, the S&P/TSX Composite Index was up 0.86% after a 1.7% rise last week. In the U.S., the Dow Jones Industrial Average increased 0.31% and the S&P 500 Index advanced 1.79% after rising 5.5% and 6.2% respectively last week. However, the S&P 500 Index is still down about 4.7% year-to-date.

- The Canadian dollar was higher again this week moving back above 80 cents, closing at 80.15 cents vs 79.33 cents USD last Friday, after rising $0.87 last week for a two week gain of 2.15%.

- Oil prices were up strongly this week, after falling about 3% last week. U.S. West Texas crude closed at $113.18 vs $103.09 USD last Friday for a 9.8% gain. Oil is now up 21% month-to-date.

- The price of gold rebounded 1.34% this week, after dropping 2.6% last week, closing at $1959.80 vs $1933.90 last Friday.

- The EU strikes gas deal with the U.S. as it seeks to cut its reliance on Russian oil. President Biden and European Commissioner President Ursula von der Leyen announced the formation of a joint task force to bolster energy security for Ukraine and the EU for the next two winters. This comes amid heightened concern that energy-importing countries continue to support Putin with oil and gas revenue on a daily basis.

- Canada has announced plans to boost oil exports as countries shun Russian supply. Our country’s resources minister said Canada will increase oil and gas exports by the equivalent of 300,000 barrels a day to help nations that are trying to shift away from Russian supplies.

- The Canadian government is also in discussions with European countries about eventually supplying them with liquefied natural gas, but any export facility would need to be eventually convertible to exporting hydrogen as part of a planned pivot away from hydrocarbons. Canada, the world’s fourth-largest oil producer, faces constraints in rapidly raising output. It currently produces more than 5 million barrels a day of liquid hydrocarbons, but the country’s pipeline network for exports is limited. Calgary-based Enbridge Inc., North America’s largest pipeline company, said on March 10 that it was in discussions with the Canadian government about how to relieve the current “energy crises” but warned that pipeline systems are currently at or near capacity.

- Cannabis/marijuana stocks are furthering yesterday's gains into the close today, after the House put the MORE Act on the list of bills to be brought to House floor next week. The House bill includes measures to take marijuana off the list of federally controlled substances and eliminate criminal penalties, and while it would still need to pass the Senate and be signed by the President before becoming law, The Hill notes that Senate Majority Leader Schumer had previously said he was hoping to introduce a bill to remove the federal ban on cannabis as early as April.

- Rogers Communications Inc.’s takeover of Shaw Communications Inc. cleared one of three crucial hurdles Thursday. The Canadian Radio-television and Telecommunications Commission announced in a release that it approved the $20-billion deal, subject to certain conditions and modifications. Among the requirements applied to the deal by the CRTC, Rogers will have to pay $27.2 million in benefits into the broadcasting system, roughly five times what it originally proposed. However, experts say this is just one of three main regulatory hurdles that must be met for this deal to be finalized.

- Long-term interest rates continued to skyrocket this week. Since March 1st, the U.S. 10-year Treasury yield jumped from 1.71% to 2.5% as of the time of this writing, that is a whopping increase of 46%. Bond markets have been reeling on this rate rise, as the price of a bond is inversely related to rates. The FTSE Canada Bond Universe Index is currently down 8% total return this year alone, after falling close to 3% last year. In the U.S., right now the Bloomberg Aggregate Bond Index is tracking the worst quarterly performance for the index going all the way back to the third quarter of 1980.

- Bank of Montreal led bank losses on Wednesday, declining as much as 3.7%, after announcing that it is selling about $2.7 billion in shares to help fund its acquisition of Bank of the West from BNP Paribas SA.

- In merger activity this week, Berkshire Hathaway agreed to buy insurance company Alleghany for $11.6 Billion or $848.02 per share.

Weekly Diversion:

Many of us love to ski, but this is taking it to a whole new heights. Check out this new Sky Skying video of Red Bull Soul Flyer Fred Fugen push the limits of what’s possible. We got dizzy just watching it!

Charts of the Week:

Markets were a bit more calm this week so we wanted to focus more on last week, when history was made. For only the 5th time ever, the S&P 500 Index gained at least 1% for 4 consecutive days. This rare occurrence has, in the past, proven to be a great time to be a buyer, as a year later it has been up more than 20% every single time with an average gain of 28%.

Source: Grant Hawkridge

The green arrows below indicate exactly when these five signals occurred…

Source: Grant Hawkridge

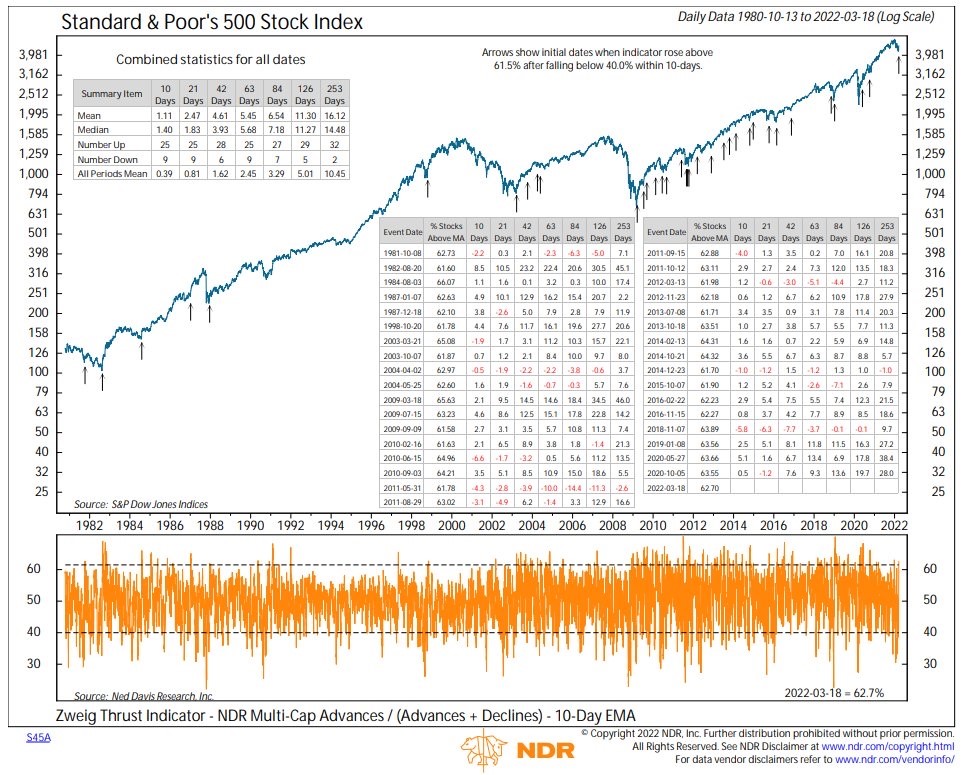

In addition to this positive sign, a couple major breadth thrusts occurred last week as well. Markets do tend to have relief rallies during corrections like the U.S. stock market is currently experiencing, but certain indicators such as breadth thrusts, which try to gauge the underlying strength/momentum of that rally and whether it is a trend change or not, are important to taken into consideration. One widely industry-followed breadth thrust indicator that we have discussed before is the Zweig Breadth Thrust Indicator. It is calculated by dividing the number of advancing issues on an exchange or index by the total number of issues (advancing + declining), and generating a 10-day moving average of this percentage. This indicator signals the start of a potential new bull market when an index moves from a level of below 40% (indicating an oversold market) to a level above 61.5% within any 10-day period.

Last Friday's rally pushed this indicator over the top when 90.5% of stocks closed above their 10-day moving averages. The chart below shows all the past instances with arrows, when this breadth thrust indicator was triggered. Since 1982, SPX has been higher 32 out of 34 times one year later with well above average results, with median and average performance of 14.5% and 16.1%. One could argue the next few month’s average performance has been even stronger illustrated in the table in the top left below. Past performance does not guarantee future results.

Source: Ned Davis Research (NDR)

Sources: CNBC.com, Globe and Mail, Financial Post, Connected Wealth, BNN Bloomberg, Canaccord Genuity, First Trust, Grant Hawkridge, Ned Davis Research Inc.