Market Insights: Oil Prices Break Slide With Strong Reversal

Milestone Wealth Management Ltd. - Aug 27, 2021

Macroeconomic and Market Developments: North American markets were positive this week. In Canada, the S&P/TSX Composite Index was up 1.46%. In the US, the Dow Jones Industrial Average increased 0.96% and the S&P 500 Index was up 1.53%, closing above

Macroeconomic and Market Developments:

- North American markets were positive this week. In Canada, the S&P/TSX Composite Index was up 1.46%. In the US, the Dow Jones Industrial Average increased 0.96% and the S&P 500 Index was up 1.53%, closing above 4,500 for the first time.

- The Canadian dollar strongly recovered this week, closing at 79.25 compared to 77.97 cents last Friday.

- Oil prices also recovered dramatically this week. US West Texas crude closed at $68.73 vs $62.14 last week, and the Western Canadian Select price closed at $56.37 vs $49.07 last week.

- Gold prices were positive this week, closing at $1,820 vs $1,784 last Friday.

- On Monday, it was announced that Pfizer Inc. (PFE) and Canadian company Trillium Therapeutics (TRIL) have entered into a definitive agreement under which Pfizer will acquire all outstanding shares of Trillium not already owned by Pfizer for an implied equity value of $2.26 billion (US$18.50 per share) in cash. The deal represents a 118% premium to the 60-day weighted average price for Trillium.

- The big six Canadian banks released their earnings this week and, unsurprisingly, all beat estimates as the banks continue to reduce their reserves for loan losses that had been set aside in the wake of the pandemic. On Tuesday, Bank of Nova Scotia (BNS) beat expectations by reporting C$2.01 excluding special items vs C$1.90 estimated, but revenue came in lower than expectations; and Bank of Montreal (BMO) crushed estimates with adjusted earnings of C$3.44 vs C$2.93 expected. On Wednesday, National Bank (NA) reported better than expected earnings of C$2.36 vs C$2.12 expectations and Royal Bank (RY) reported better than expected earnings of C$2.97 vs the expected C$2.70. On Thursday, Toronto-Dominion Bank (TD) beat estimates with adjusted earnings of C$1.96 vs C$1.92 and CIBC (CM) reported adjusted earnings of C$3.93, beating estimates of C$3.41.

- Canada’s Alimentation Couche-Tard (ATD.b), owner of convenience stores such as Winks, announced that it is to acquire convenience stores from ARS Fresno LLC and certain affiliated companies which includes 35 high quality locations currently operated under the Porter's brand and located predominately in Oregon and Western Washington.

- US Real GDP growth in Q2 was revised up to a 6.6% annual rate from a prior estimate of 6.5%, slightly below the 6.7% expected. Net exports and business investment were revised upwards, while inventories and residential investment were revised downwards. The largest positive contributions to the real GDP growth rate in Q2 were consumer spending and business investment.

- The preferred inflation measure of the US Federal Reserve, the Personal Consumption Expenditures (PCE) Index rose 0.4% in July and is now up 4.2% year-over-year. While the massive impact of shutdowns last year muddies the inflation picture, a look at price pressures over the past six months (which reduces the "base effect" impact), shows an even more profound rise in inflation, with overall PCE prices up at a 5.9% annualized rate.

- The US Federal Reserve held its annual Jackson Hole summit this week (virtually for the second year). On Friday, Fed Chairman Jerome Powell’s summary speech indicated Friday that the central bank is likely to begin tapering before the end of the year. However, he said that interest rate hikes are not imminent as there is still “much ground to cover” before the economy hits full employment. The markets seemed to take the speech in stride with US stock markets positive on Friday and interest rates in the bond market only marginally lower.

- Here is a link to a short video from Canaccord’s chief U.S. Strategist Tony Dwyer entitled What Market Are You Referring To: DWYER VLOG

Weekly Diversion:

Check out this video of a pretty ingenious musical instrument.

Charts of the Week:

This week we will focus on the energy sector which is always a relevant topic here in Calgary. Crude oil prices have already had a very strong year, with West Texas Intermediate (WTI) prices up 43% YTD and the S&P/TSX Capped Energy Price Index up 36% YTD. Perhaps this uptrend has had a positive effect on Calgary real estate prices, where the Teranet/National Bank House Price Index for Calgary is up about 7% YTD, finally pushing above its prior all-time peak from October 2014. On Monday, WTI prices increased over 5%, kickstarting a strong week for oil prices (+10.6%), partially reversing a large slide in prices (17% drop since early July peak). In fact, until this week, oil prices had declined in the previous seven straight trading days. The following chart shows each of these past ending streaks with a red dot including this week. The last time we saw this occur was in February 2016, after which there was a very strong push higher in prices and equity returns.

Source: Bespoke Investment Group

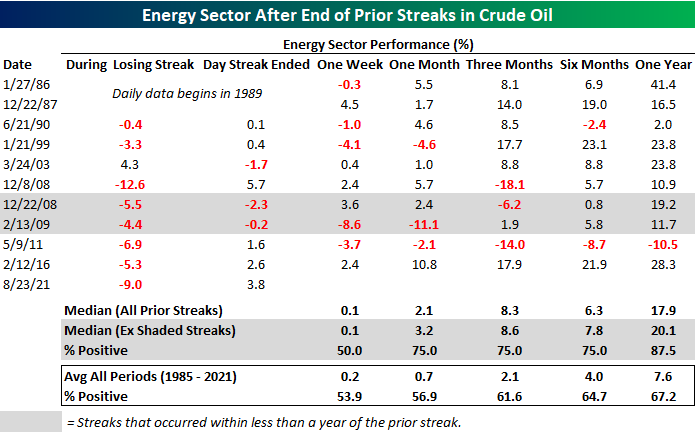

The 5%+ gain on Monday is not overly significant in itself, but what is rare is that this 5%+ gain marked just the 11th time since 1985 where the commodity ended a 5+ day losing streak with a gain of over 5%. This oddity is far from a large enough sample size to make any forecasts, but it is interesting to see what has happened in previous instances. In prior signals such as this, oil prices had above average returns, but they weren’t particularly consistent. Energy sector stocks, on the other hand, followed up with better than average returns but also the consistency of those positive returns was better than the long-term average.

The next two tables show what has occurred to oil prices and energy sector equity returns, depicted by the US energy sector in this case, after these signals occurred over varying time periods up to a year. The first table on oil prices clearly shows an extremely strong price outlook with 6-10 times stronger median returns over the next 6 to 12 month than all other periods. However, if you remove the 2008/9 outlier period which was the rebound after the Great Recession (grey shaded lines), the WTI performance was still strong but less consistent with only a 50% chance of a positive return over the next six months. The second table on energy sector returns, with also omitting the 2008/9 period, shows not only a strong return outlook over all periods but also a more consistent pattern with a percentage positive rate of 87.5% over the following year. In fact, one year later the median energy sector return was over 20% vs. just 7.6% over all other periods with just one negative instance in the past ten. Let’s hope this pattern holds true again this time.

Source: Bespoke Investment Group

Sources: CNBC.com, Globe and Mail, Financial Post, BNN Bloomberg, Tony Dwyer, Canaccord Genuity, First Trust, Bespoke Investment Group