Market Insights: Flip Flop Season

Milestone Wealth Management Ltd. - Jun 25, 2021

Macroeconomic and Market Developments: Stock markets in North America were up significantly this week. In Canada, the S&P/TSX Composite rose 1.15%. In the US, the Dow Jones Industrial Average was up 3.44% and the S&P 500 Index increased 2.74%. The

Macroeconomic and Market Developments:

- Stock markets in North America were up significantly this week. In Canada, the S&P/TSX Composite rose 1.15%. In the US, the Dow Jones Industrial Average was up 3.44% and the S&P 500 Index increased 2.74%. The S&P 500 fully reversed last week’s steep decline to climb to a new all-time high.

- The Canadian dollar was up over a cent this week, closing at 81.33 cents vs 80.22 cents last Friday.

- Oil prices were also strong this week, with US West Texas crude finishing at $74.04 vs $71.29 USD last week, and the Canadian WCS price at ~$60.12 vs ~$58.10 last week.

- Gold prices were up slightly this week, closing at ~$1,782 vs ~$1,769 last Friday.

- Yesterday, Microsoft joined Apple in the exclusive $2 trillion club. Yes, there are now two companies valued over $2 trillion, and two between $1-2 trillion.

- Equities received a lift on Thursday as Joe Biden confirmed an infrastructure agreement has been approved by a bipartisan group of senators. The spend will be $1.2 trillion over the next 8 years. Metals and oil rose on the news, but have since settled back down. While the bill is not officially passed, the agreement adds some strength to an already strong economic growth outlook. However, the agreement faces a complicated path to approval given insistence from progressives and the White House that the Senate also pass a separate package via reconciliation that includes Democratic priorities.

- US economic data released this week included the final GDP number for the first quarter, confirmed at 6.4% quarter over quarter at an annual rate (unchanged from the last estimate). The Personal Consumption Expenditure component was adjusted up slightly from 11.3% to 11.4% annual rate.

- The US Federal Reserve was the other high-profile topic, with some discussion about differing views in this week's commentary regarding inflation risk and the start of the policy normalization process. No surprise at all that banks passed the Fed stress test, and the Fed said it would end temporary limits on dividends and buybacks.

- Christine Lagarde, President of European Central Bank, told EU leaders that the Eurozone economy will to return to pre-Covid levels by Q1 2022, with inflation to increase further, but only on temporary factors.

- In Canada, the highlight this week was Wednesday's retail sales report. Canadian retail sales fell 5.7% in April, a larger drop than the 5.1% consensus and StatCan's early estimate. The agency provided a preliminary estimate for May retail with sales down 3.2%. A soft patch was widely expected given third-wave lockdowns, but was tempered by confidence growing for a strong summer recovery already underway, aided by faster vaccine progress and a much-improved COVID picture. We have a somewhat busier week ahead on the Canadian macro calendar with April GDP to be announced on Wednesday.

- Here is a link to a short video from Canaccord’s chief U.S. Strategist Tony Dwyer entitled It’s All Relative – Indicator Still Points to Value: DWYER VLOG

- For a deeper dive, the US investment company First Trust has put out a US COVID-19 Tracker. Click here: COVID TRACKER

- In addition, First Trust has created a COVID Recovery Tracker. Click here: RECOVERY TRACKER

Weekly Diversion:

For a bit of fun this week, in honor of Conan O’Brien’s last episode which aired last night, here is one of the best moments from the past where he had his dopplegänger on the show.

Charts of the Week:

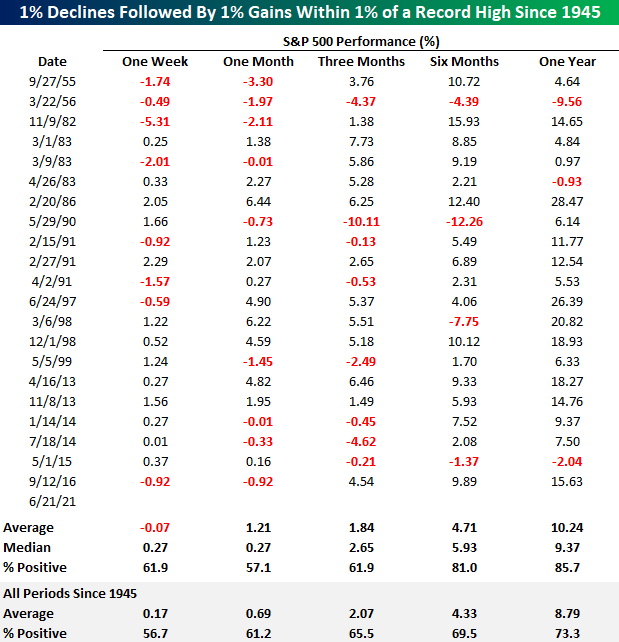

There has been a lot of ‘flip-flopping’ in the markets over these last many days. On Monday, the US had its strongest breadth days in over a year, which followed a negative all-or-nothing day last Friday. The S&P 500 closed out last week by falling 1.3% on Friday, but then rebounded 1.4% this Monday to kick off the week on a positive note. Perhaps this is a good sign for the US market which, for the most part, had been in a choppy sideways pattern with no upward movement since mid-April. Although back-to-back 1% moves up or down in the market are not uncommon, what is unique is when this occurs so close to an all-time high. In fact, in the post-WWII period, there have only be 21 prior occurrences where the S&P 500 has fallen more than 1% after closing within 1% of a record high, just to rebound over 1% the following day. One may think that this type of volatility is a sign of instability and potentially a warning sign, so let’s take a look at the numbers to see if that has been the case in the past. The following chart highlights the seven times this has occurred in the last 10 years, including this week. Looking at all instances, the table below summarizes how markets fared over the following year after each ‘flip-flop’. In general, the average returns point to marginally below average returns over the following three months, but slightly above average over the next six. One year out, returns on average have been better than all other periods of time by about 1.5%. Therefore, while the return numbers following a ‘flip-flop’ don’t show any meaningful forward-looking outperformance relative to other periods, it also doesn’t support the idea that this type of volatility near an all-time high is negative signal.

Source: Bespoke Investment Group

Sources: CNBC.com, Globe and Mail, Financial Post, BNN Bloomberg, Tony Dwyer, Canaccord Genuity, First Trust Advisors, Bespoke Investment Group, CNN