Market Insights: "If the Troops Will Lead, the Generals Will Follow"

Milestone Wealth Management Ltd. - Dec 11, 2020

Macroeconomic and Market Developments: North American stock markets were mixed this week. In Canada, the TSX Composite index was slightly positive, up 0.15%. For US markets, the Dow was down 0.57% and the S&P500 was down 0.97%. The Canadian dollar

Macroeconomic and Market Developments:

- North American stock markets were mixed this week. In Canada, the TSX Composite index was slightly positive, up 0.15%. For US markets, the Dow was down 0.57% and the S&P500 was down 0.97%.

- The Canadian dollar was flat this week, staying at 78.3 cents.

- Oil prices were mostly flat with West Texas crude up slightly from $46.00 to $46.50 this Friday. Western Canadian Select oil held steady at $33.00, the same as last week.

- Gold was up slightly this week, finishing at $1,843, up from $1,840 last week.

- A 90-year old woman in Britain became the first person to receive the Pfizer-BioNTech vaccine for COVID-19 on Tuesday. Britain became the first country to approve the Pfizer-BioNTech vaccine last week, and the U.K. has ordered 40 million doses. The vaccine requires two doses, 21 days apart. In Canada, Ontario is set to receive 6,000 doses next week and will start immunizing health workers in Ottawa and Toronto on Tuesday.

- Calgary based junior oil and gas company Cardinal Energy (CJ) revealed that legendary Calgary billionaire Murray Edwards invested more than $13 million into a recent convertible debt issue. This news led to a sharp rise in the company’s stock this week as investors interpreted this as a positive sign for the company. Edwards currently owns 9.6% of Cardinal.

- Whitecap Resources (WCP) announced that it is buying TORC Oil & Gas (TOG) in all-stock transaction valuing TORC at about $552 million plus assuming $335 million of debt. Shareholders of TORC will receive 0.57 Whitecap common shares in exchange for each TORC common share.

- This week saw two very popular US tech companies go public. Popular food delivery service DoorDash (symbol DASH) completed its IPO on the NASDAQ market in the US on Wednesday. The highly sought-after IPO was priced at US$102.00 and the stock closed the first day of trading at US$189.51. On Thursday, AirBNB (symbol ABNB) completed its long-anticipated IPO as well. The IPO was priced at US$68.00 and closed the first day at US$144.71.

- Ongoing negotiations in the US government regarding the next round of stimulus seem to have stalled once again. Congress remains at an impasse over a coronavirus stimulus package. Republican Senate leaders rejected a $908 billion aid package, which had been proposed by a bipartisan group of lawmakers.

- Total global COVID-19 cases continued to rise, hitting just over 70.0 million, with total deaths at roughly 1.59 million. In Canada, total cases climbed to 442,069, with active cases sitting at 73,225. In Alberta, total cases are at 75,054, and active cases are now at 20,163.

- For a deeper dive, the US investment company First Trust has put out a US COVID-19 Tracker. Click here: COVID TRACKER

Charts of the Week:

We have mentioned the strength of U.S. large cap technology a few times over the last weeks and months, and as a result, extreme divergence of the S&P 500 market-weighted vs. equal-weighted indices. This can work well for periods of time for passive index followers but it isn't always an indication of underlying strength.

However, recently, we have seen strength from small cap companies with their recent breakout to new highs. We have also seen some similar characteristics with Canadian small and mid-cap companies. We view this as an indication of strong overall breadth for the North American stock market and a positive forward-looking indicator.

The notion that a healthy market is one in which the smaller stocks are the leaders has both an anecdotal and a statistical basis. The anecdotal basis traces to sayings such as “if the troops will lead, the generals will follow,” which used to be widely quoted on Wall Street, especially during the “Nifty Fifty” era of the late 1960s and early 1970s. The reference to the “generals” was to the biggest of blue-chip stocks such as General Electric GE and General Motors GM, which at the time were among the largest-cap stocks in the market.

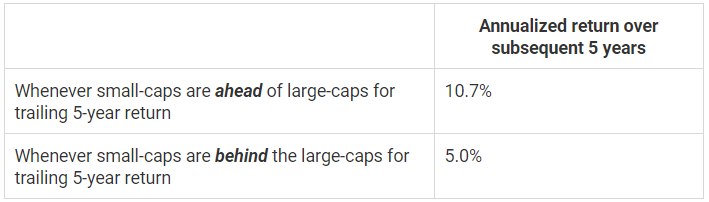

There also is statistical support for this notion. There has been a distinct tendency since 1970 for the stock market to perform better whenever the small-caps are beating the large-caps over the trailing five-years (as shown in the table below with data through 2019):

Source: TheStreet Inc., www.thestreet.com

The Russell 2000 Index is the primary small cap index in the U.S. To illustrate the recent strength of this market, the following chart shows its recent multi-month breakout, its third over the past 15 years. We view this as a potentially significant development. It is interesting to note that the last two prior breakouts occurred shortly after presidential elections. The prior two post-election rallies (2012 & 2016) lasted about two years and ran about 45% and 35% respectively. With the index currently around the 1900 level, if history repeats itself, it will indicate a two-year target of 2300-2400. Small cap companies have not performed relatively well the last few years, but this new breakout could be an indication that the troops are finally leading, which as history has shown is a positive for overall markets. This could be a good sign for the small to mid-cap Canadian markets as well (we include mid-caps for Canada as many mid-caps in Canada would be classified as small caps in the US).

Source: @yuriymatso

Sources: CNBC.com, Globe and Mail, Financial Post, Government of Canada, Government of Alberta, Johns Hopkins, oilprice.com, Canaccord Genuity, TheStreetInc., @yuriymatso