Market Insights: First Quarter wrap-up

Milestone Wealth Management Ltd. - Apr 14, 2016

The first quarter of 2016 was a roller coaster for stock markets around the world. Not only were most major country stock indices down more than 10% year-to-date at some point in the quarter, we also witnessed very high daily volatility. Almost 43%

First Quarter wrap-up

The first quarter of 2016 was a roller coaster for stock markets around the world. Not only were most major country stock indices down more than 10% year-to-date at some point in the quarter, we also witnessed very high daily volatility. Almost 43% of the trading days saw movements of greater than 1% (up or down) in the S&P500 index. This ranks as the sixth highest share of days in the first quarter of the year since 1951, and if you remove those times in a recession, it was the third highest on record.

Here in Canada, the TSX Composite has been on a wild ride of its own. The composite peaked out at 15658 (closing basis) back in September 2014 and fell to a bottom of 11843 on January 20th for a price decline of over 24% and a bear market. A bear market is defined as any decline from a high of more than 20%. Since then it has bounced back 14% in just eleven weeks to finish the quarter with a positive 3.7% price return. Although impressive, the composite is still down almost 14% from its 2014 all-time high.

The S&P500 never did enter an official bear market and its current position is only 3.3% below its May 2015 all-time high. That being said, the relative result has been skewed by a few large cap stocks, and thus the breadth of their market has not been nearly as strong. If you look at all market capitalizations in the U.S., the 'mean' stock did enter a bear market (down over 20% from the peak) and is still down about 8% from its high.

Globally, overall markets, as defined by the MSCI World Price Index (local currency), were down as much as 18.4% from their May 2015 all-time high to a February 11th low. These markets bounced back up 11.5% to close the first quarter down 2.5% on the year.

For Canadians, one of the biggest themes this quarter has been an appreciating Loonie, which saw a rise of 6.4% against the Greenback and over 13% from the January 19th intra-day low. From a global portfolio management perspective, this can be a detriment to returns if currency is unhedged. To illustrate, although the S&P500 price index was up 0.8% on the quarter, it was down over 5% in Canadian dollars. Internationally, the MSCI EAFE price index was down over 10% in Canadian dollars which is far worse than the underlying index in local currency.

Fixed income markets saw a boost from declining long term interest rates with the FTSE TMX Canadian Bond Universe index up 1.4%. High yield markets also performed reasonably well, bouncing off of depressed levels.

In the commodity complex, WTI Crude Oil price finished the quarter off $1.64USD but has seen a nice rise in the past couple of weeks here in April. From both a fundamental and technical perspective, the price of oil does seem to be in the process of carving a long-term bottom. We will need further evidence of this over the coming weeks, but we may receive confirmation soon with two important upcoming OPEC meetings on April 17th and June 2nd to consider a production freeze.

We have discussed over the last couple of quarters that our long-term strategic asset allocation hasn't changed a great deal due to the fact that we view recession risk for the U.S. to remain a low probability in the near-term. Our internal Milestone recession risk composite has yet to flash red and we have seen some improvement since mid-February. In addition, our fundamentally driven intermediate-term positive view on markets remains intact. That being said, declining U.S. retail sales of late are a concern, so this is an area we will continue to watch closely. Year-over-year corporate earnings results have been very poor of late; however, over the coming quarters we feel earnings expectations will become much less onerous when compared to the previous year and this may result in more upside surprises.

From a technical perspective, we wish to point out that a rare 'breadth thrust' signal was triggered at the end of March. Although looking at any indicator or signal in isolation is typically not generally very meaningful, this is a signal that may have more bearing. This signal occurs when over 90% of the market is trading above their 50-day moving averages. The chart below from Ned Davis Research shows all past occurrences of this signal (see arrows underneath the blue line). They use a multi-cap series that includes about 97% of total U.S. market cap). As you can see, this signal typically has occurred prior to significant advances. We are hopeful that this time will be no different.

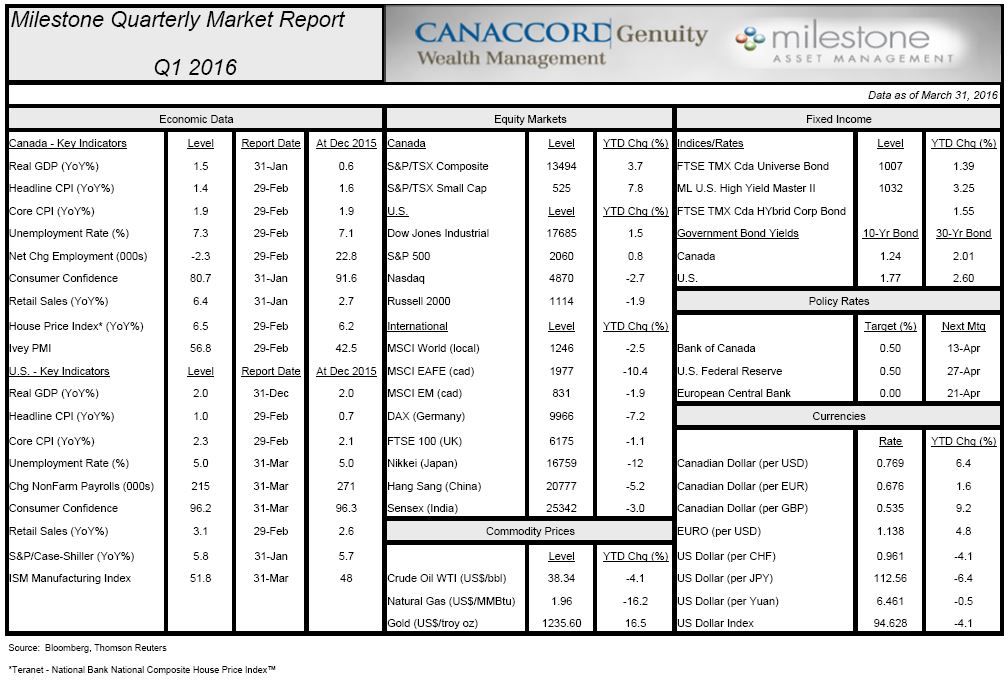

Here is our Milestone Market Report on economic data, capital markets, commodities and currencies through March 31st, 2016: