Market Insights: Why invest overseas?

Milestone Wealth Management Ltd. - Jul 30, 2015

We thought it would be beneficial to share some of our insights on international equity investing. It is our belief that there are certainly benefits to having an overseas equity exposure in a balanced or equity mandate.

Is there a benefit to investing in equities overseas?

We thought it would be beneficial to share some of our insights on international equity investing. It is our belief that there are certainly benefits to having an overseas equity exposure in a balanced or equity mandate. In fact, international exposure in our portfolios has always been a component of our portfolio construction and likely always will. One might ask, with somewhere on the order of 40% of S&P 500 company revenues coming from foreign sources, can you not obtain overseas exposure through large-cap U.S. stocks? With high correlation between domestic and foreign equities, does adding international exposure really actually improve diversification? These are both good questions and we hope, in a short amount of space, to clarify why we believe it is important to have this exposure.

In our view, international exposure not only adds geographic diversification, it adds exposure to different companies, sector and industry weightings, and currencies and a cultural element that is often overlooked. From geopolitical risks to simply how different cultures invest, different regions of the world are rarely fully in sync even with world commerce becoming more globalized than ever. Below is a chart showing the industry breakdowns of the MSCI EAFE covering Europe, Australasia & Far East Index (EFA), the S&P 500 (SPY) and the MSCI Emerging Markets Index (EEM). The industry exposure varies widely between the regions. We have left the TSX Composite off this particular illustration as the S&P 500 is a much larger world representative; however, our market also varies greatly in that energy makes up over 20% or roughly three to four times more than these regions.

(Source: Morningstar)

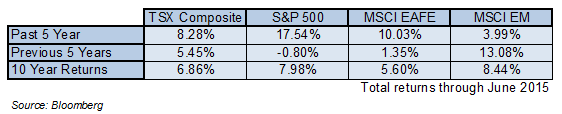

While correlations between the S&P 500 and the MSCI EAFE have been moving higher over the years, it is important to differentiate between markets moving roughly together and actual market returns. From the 1970s through 1990s, the five-year rolling correlation between these two markets varied between 0.3 and 0.7. Starting about fifteen years ago, this changed significantly, and over the past ten years we have seen correlations more in the 0.8-0.9 range globally. Correlation is measured from -1 to +1, with -1 being perfectly negative correlated, 0 being no correlation and +1 being perfectly correlated. Therefore, one may say that domestic and international equity markets have had fairly high correlation in the last ten to fifteen years. This does not translate, however, into similar returns:

As you can see, there is a wide dispersion of returns over five-year periods (even more so in shorter terms). In the last five years, there has been a very large discrepancy between all market regions, with U.S. equity markets being the clear winner. The previous five years we saw the opposite, with U.S. markets actually declining and EM markets performing very well. From glancing at the numbers, it appears our market (TSX Composite) has been fairly stable. This is also deceiving since the TSX Composite has recently significantly underperformed compared to both the S&P500 and the MSCI EAFE.

It is true that over very long periods of time the performance of different equity markets (Canada, U.S., International and Emerging) become more in line with each other. However, for individual investors, ten or more years is not a realistic time frame to judge diversification benefits or returns. Periods of three to five years is likely more in line with what most consider longer-term evaluation metrics. International equity exposure will improve diversification and help smooth returns out through rebalancing over time frames that are in line with most individual investors and their objectives.

Disclaimer: This newsletter is solely the work of the author for the private information of clients. Although the author is a registered Investment Advisor at Canaccord Genuity Corp., this is not an official publication of Canaccord Genuity Corp. and the author is not a Canaccord Genuity Corp. analyst. The views (including any recommendations) expressed in this newsletter are those of the author alone, and are not necessarily those of Canaccord Genuity Corp. The information contained in this newsletter is drawn from sources believed to be reliable, but the accuracy and completeness of the information is not guaranteed, nor in providing it do the author or Canaccord Genuity Corp. assume any liability. This information is given as of the date appearing on this newsletter, and neither the author nor Canaccord Genuity Corp. assume any obligation to update the information or advise on further developments relating to information provided herein. This newsletter is intended for distribution in those jurisdictions where both the author and Canaccord Genuity Corp. are registered to do business in securities. Any distribution or dissemination of this newsletter in any other jurisdictions is prohibited. The holdings of the author, Canaccord Genuity Corp., its affiliated companies and holdings of their respective directors, officers and employees and companies with which they are associated may, from time to time, include the securities mentioned in this newsletter.