Market Insights: Second Quarter Wrap-up

Milestone Wealth Management Ltd. - Jul 09, 2026

Key Updates on the Economy & Markets

Equities staged a strong recovery in Q2, with the S&P 500 Index rising 14.9% and finishing near record highs, after a 4.6% decline in the first quarter, while the S&P/TSX Composite increased 6.4% in Q2. The Middle East conflict and oil shock that started in Q1 continued for most of Q2, but oil prices fell as the two sides worked toward a ceasefire agreement. Meanwhile, investors’ enthusiasm for artificial intelligence (AI) stocks returned, fueling a rally in semiconductor stocks. As companies reported strong Q1 earnings, the gains broadened beyond technology to include mid-and small-cap stocks. Even as stocks rallied, market conditions continued to evolve. The spring rise in oil prices lifted inflation to a three-year high, and the US Federal Reserve (Fed) signaled a shift from rate cuts to rate hikes. In this letter, we recap the key developments in Q2, discuss the oil reversal and its impact on Fed policy, analyze the rally in semiconductor stocks, and look ahead to Q3.

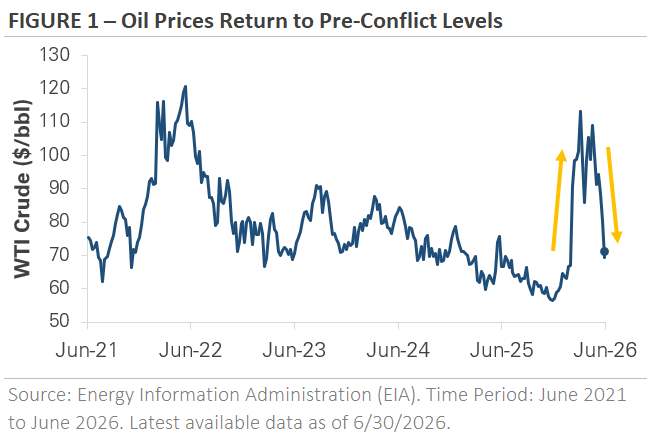

Oil Prices Return to Pre-Conflict Levels

The energy shock that started in the first quarter unwound almost as fast as it arrived. Figure 1 shows oil peaked near $115 in early April as the Middle East conflict closed the Strait of Hormuz, disrupting global oil supply. Energy prices remained volatile throughout the quarter, but oil ended Q2 near $70 USD, returning to where it traded when the conflict began. The decline followed a ceasefire between the U.S. and Iran and expectations for the Strait, which carries nearly 20% of the world's oil, to reopen. Gas prices followed the same path, rising sharply during the spring before falling in late Q2.

The price reversal matters because energy prices feed directly into inflation, which in turn shapes the outlook for interest rates. When oil spiked earlier this year, inflation followed. Consumer prices (inflation rate) in the US rose 4.2% year-over-year in May (3.2% for Canada), the highest in three years, with over half of the monthly increase tied to energy. Excluding energy, the core rate was 2.9% (2.2% for Canada), an indication that the rise in inflation was driven by oil rather than broad price pressures.

The oil price spike and the subsequent rise in inflation reshaped the interest rate outlook. Coming into this year, the market expected the Fed to cut interest rates two or three times. During Q2, the market swung from expecting rate cuts to pricing in a rate hike this fall. The Fed held interest rates steady at both of its meetings during Q2, but it leaned toward the market's view, signaling that its next move could be up rather than down.

The May inflation reading is backward-looking, so it captures oil near its peak rather than where it sits today. With oil back at pre-conflict levels, the main driver of higher inflation has started to fade, and inflation is expected to ease in the months ahead. What stands out for the full quarter is how the market handled the episode. There were stretches of volatility as the conflict dominated headlines in the spring, but stocks moved past them and finished Q2 higher.

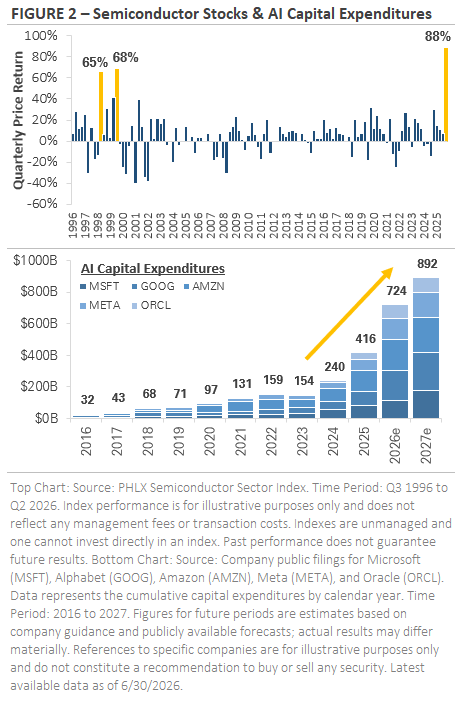

AI Spending Fuels Semiconductor Stock Rally

Semiconductor stocks led the US market's advance, posting their strongest quarter in nearly 30 years. The top chart in Figure 2 graphs the quarterly price return of the semiconductor stock index, with Q2 towering over nearly everything before it. The group returned 88% for the quarter and was up nearly 100% before pulling back in the final weeks of June. The only comparable quarters occurred in the late 1990s, when the internet went mainstream.

The rally is anchored to a wave of technology investment, with much of the money flowing to the chipmakers. The bottom chart graphs the combined capital spending of five of the largest tech companies building AI infrastructure: Microsoft, Amazon, Meta, Alphabet, and Oracle. The group spent a combined $32 billion USD in 2016. By 2025, that figure had grown to roughly $416 billion. The pace continues to climb: the five companies are projected to spend about $724 billion this year and nearly $900 billion next year. The capital expenditures pay for data centers, the computer chips inside them, and the equipment and power to run it all. The companies leading the buildout are reporting record earnings and growing backlogs, and many say they're limited more by how fast they can build than by demand.

The surge in spending is also reshaping financial markets. Private companies are going public to fund their spending, while public companies are turning to debt and equity markets to finance their buildout. SpaceX completed the largest IPO in history during Q2, raising $85 billion. Other well-known private companies, including OpenAI and Anthropic, are expected to follow over the next year. In the public market, companies such as Alphabet and Oracle are issuing both stock and bonds to fund their spending. The amount of money being raised, and the spending plans behind it, point to a buildout that is still expanding.

A move of this size, both the spending and the share price gains, is historic. The market is treating AI as a major technological shift, and the quarter brought increased spending and earnings growth, with companies signaling more spending ahead. At the same time, a quarter like this shows how much future growth is already priced in. The closest historical parallel, the late 1990s, points to what rapid transformation tends to bring: both real opportunity and high expectations.

Market Breadth Remains Strong Beyond Tech

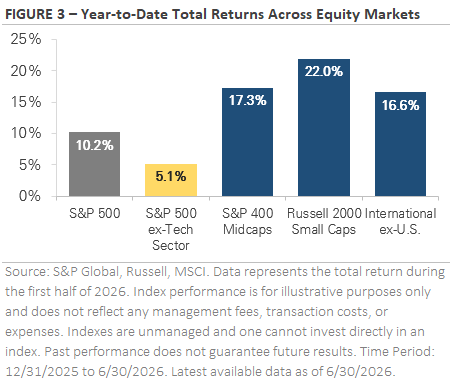

Beneath the headline rally in tech, Q2's gains were broad. Figure 3 on the following page compares year-to-date returns across the market. The S&P 500 has returned 10.2% this year (11.2% for the S&P/TSX Composite) but strip out the technology sector and that falls to just 5.1%, an indication of how much of the index's return has come from a single sector. The remaining market segments in the chart produced double-digit returns, outperforming the S&P 500. The S&P 400, an index of US mid-cap stocks, and international stocks have both returned approximately 17%, while the US small-cap Russell 2000 has gained 22%. For most of the past few years, the stock market's gains were concentrated in a handful of mega-cap tech stocks. Market leadership has broadened this year, creating a more balanced market.

Several developments explain why the rest of the market has started to outperform. The first is profitability. Smaller companies’ profit margins weakened in 2022 and 2023 as inflation spiked and the Fed raised interest rates. Small caps tend to carry more floating-rate debt, so as the Fed cut rates in recent years, the interest savings flowed to their bottom line. The second is the economy. Smaller companies are more sensitive to domestic economic conditions, so the economy's resilience has been a direct tailwind. There were concerns that this year's oil shock would weigh on the global economy like past oil crises. However, today's economy depends far less on energy than it did in the 1970s, and the impact has so far been relatively contained. The third is valuation. After years of tech stocks leading the market, smaller companies look cheaper by comparison, and their

improving earnings have made that gap harder to overlook.

No single factor explains the shift, but together they make a fundamental case for why the gap has started to close. Profit margins are improving, the economy continues to expand, and parts of the market trade at valuation discounts. As this year has shown, holding a mix of company sizes, styles, and geography means not depending on any single part of the market to do well.

Equity Market Recap – Key Trends During Q2

Equity markets traded higher throughout the quarter, with most of the advance coming in April as stocks rebounded from their late-March lows. The

strength carried into May, with the S&P 500 posting a nine-week winning streak into month end. The index set a record high in early June before giving back some ground to finish up with a 15.2% Q2 return, its strongest quarter since Q2 2020, the early stages of the pandemic recovery. The Nasdaq gained 27.7% on the quarter as tech stocks led the market rally, while the Dow returned 13.4%. As mentioned in the prior section, market breadth remained strong during the quarter. Smaller companies outperformed most major indexes, with the Russell 2000 gaining 21.5%. Our S&P/TSX Composite returned 7% in Q2.

From a sector perspective, nine of the eleven S&P 500 sectors finished higher. However, technology was the only sector to outperform the broad index, with a gain of 31.8%. Of the remaining sectors, Industrials, Consumer Discretionary, and Financials each rose 9% or more, while defensive sectors such as Utilities and Consumer Staples were flat. Energy was the only sector to trade lower, falling 13.4% as oil prices returned to pre-conflict levels. In Canada, the strongest sector in Q2 was the S&P/TSX Capped Financials total return gaining 23.2%, while the weakest were the S&P/TSX Capped Energy and Materials sectors losing 11.4% and 11.5%, respectively.

International markets advanced alongside U.S. stocks, with the same divide between tech stocks and the rest of the market showing up overseas. Emerging markets returned nearly 24.1% in USD, as Asian markets like South Korea and Taiwan benefited from the same semiconductor rally as in the U.S. Developed markets gained 11.1% but trailed both emerging and U.S. stocks due to their lighter tech exposure.

Credit Recap – Bonds Trade Higher Despite Interest Rate Volatility

The bond market had another volatile quarter as interest rates tracked the path of oil. US Treasury yields rose early during the quarter as oil prices = remained elevated and the odds of a rate cut weakened, then reversed lower in June as energy prices declined and the inflation outlook improved. The 30-year Treasury was especially volatile, rising to its highest level since 2007 over concerns about oil, inflation, and a Fed leaning toward higher rates. Shorter-term yields, which are the most sensitive to Fed policy, also increased over the quarter as the market priced out additional rate cuts and began to weigh the possibility of a rate hike.

By the end of the quarter, the volatility had eased and yields stabilized. The S&P US Aggregate Bond, a broad index of U.S. investment-grade bonds, returned 0.8% for the full quarter and now 0.85% YTD. Corporate bonds outperformed during Q2, with high yield gaining 2.4% and investment-grade returning 1.8%. In Canada, our S&P Aggregate Bond Index returned a much stronger 2% in Q2 and up 2.23% YTD. Credit spreads, which measure the difference in yield between corporate and government bonds, retightened after widening in the spring as oil prices rose. Overall, credit spreads remain tight by historical standards, signaling continued confidence rather than concern. The one exception is the lowest-quality corner of the high-yield market, where CCC-rated bonds haven't recovered to pre-conflict levels, an indication of some caution toward the weakest borrowers.

Loonie Losing Some Ground

We will finish off by noting that the Loonie has lost further ground to the US dollar this quarter, falling 2% on a relative basis, and is now down 3.3% YTD against the Greenback. The decline this quarter mainly reflects weaker oil prices since May dragging on Canada's trade balance, combined with widening interest-rate differentials as the Bank of Canada's dovish stance contrasts with a more resilient US economy and Fed. Softer Canadian jobs/growth data and broader US-dollar strength (plus recent CUSMA/trade-renegotiation uncertainty) have added to the pressure.

2026 Outlook – What to Watch in Q3

Stocks ended Q2 near all-time highs as they rebounded from the volatility earlier this year. The conflict behind that volatility isn't fully resolved, but oil prices have fallen back to pre-conflict levels. There were concerns the oil spike would slow down the global economy, like past energy crises, but the economy has held up so far with few signs of significant stress. What's left is a set of open questions: the path of oil and inflation, the durability of the AI investment cycle, and whether the market's broadening continues. The remainder of this year will be shaped by how each plays out.

The first is the path of inflation and interest rates. With oil back near where it started, inflation is widely expected to ease. The question is whether the cooling shows up in the coming inflation reports. If it does, it would take some pressure off the Fed. If inflation remains elevated, the Fed's cautious stance is likely to persist, with a rate hike on the table. The next few inflation reports will go a long way toward answering what the Fed does next.

The second is the AI buildout. The spending behind it has been enormous, and the gains in the stock market have been big. The question now is whether both can hold. The AI trade has become popular, and the late-quarter pullback in technology showed how quickly stock prices can swing when expectations are high. Over time, the spending will need to translate into real profits to justify the scale, especially as a growing share of it is funded by issuing new debt and stock. The past quarter showed the promise of technology and served as a reminder of how much is already expected of it.

The third is whether the market's broadening continues. This year has been unique, with broad participation across the market existing alongside narrow leadership at the very top. Most sectors and company sizes have participated in the stock market rally, even as a small group of technology stocks has driven the largest share of the returns. The question is whether the gains keep spreading or leadership narrows again to a handful of names.

A list of open questions can naturally create some unease, so it's worth looking at how the past quarter unfolded. The market faced a war, an energy shock, inflation at a three-year high, and a Federal Reserve signaling a potential rate hike. Through all of it, stocks not only held their ground but traded to new highs. We can't know exactly how the questions will resolve, but a diversified portfolio and a long-term perspective can help navigate periods of uncertainty.

Thank you for your continued trust in Milestone and for the opportunity to assist you in working toward your financial goals. We understand the risks and opportunities facing the markets and the economy and are committed to helping you effectively navigate all investment environments by maintaining a globally diversified portfolio designed to weather the market’s swings, aligned with your long-term goals. Market volatility can be unsettling, but it’s a normal part of investing. Therefore, it’s critical to stay invested, remain patient, and stick to the plan, as we’ve collaborated with you to establish a unique, personal allocation target based on your financial position, risk tolerance, and investment timeline.

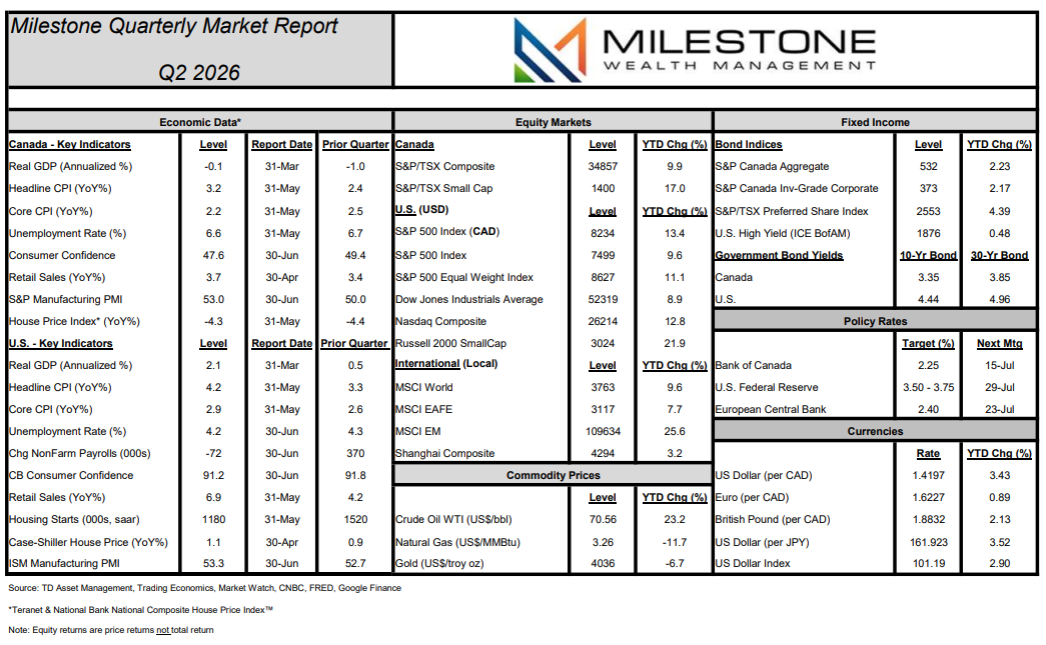

Here is our Milestone Quarterly Market Report on economic data, capital markets, commodities, and currencies through

June 30th, 2026: *Click Here For PDF Version*

Disclosure:

Investing in equities is not guaranteed, values change frequently, and past performance is not necessarily an indicator of future performance. Investors cannot invest directly in an index. Index returns do not reflect any fees, expenses, or sales charges. Opinions and estimates are written as of the date of this report and may change without notice. Any commentaries, reports or other content are provided for your information only and are not considered investment advice. Readers should not act on this information without first consulting Milestone, their investment advisor, tax advisor, financial planner, or lawyer. This communication is intended for Canadian residents only and does not constitute as an offer or solicitation by anyone in any jurisdiction in which such an offer is not allowed.

Sources: Bloomberg, Barchart, TD Asset Management, Trading Economics, Teranet & National Bank of Canada, Barchart, MarketDesk Research LLC,S&P Global, Russell Indices, MSCI, Nasdaq, PHLX Semiconductor Sector Index, Energy Information Administration (EIA), company filings for Microsoft (MSFT), Alphabet (GOOG), Amazon (AMZN), Meta (META), and Oracle (ORCL).

©2026 Milestone Wealth Management Ltd. All rights reserved