Market Insights: Nuclear Power’s Return & What It Could Mean for Uranium Demand

Milestone Wealth Management Ltd. - Jul 03, 2026

Macroeconomic and Market Developments:

- North American markets were up this week. In Canada, the S&P/TSX Composite Index moved up by 1.22%, while in the U.S., the Dow Jones Industrial Average increased by 1.89% and the S&P 500 Index rose 1.71% after a steep decline in the Tech sector.

- The Canadian Dollar was stagnant this week, closing at 70.39 vs. 70.46 cents USD last week.

- Oil prices dropped again this week, with U.S. West Texas Crude closing at US$68.78 vs. US$69.38 last week.

- The price of Gold rose this week closing at US$4,187 vs. US$4,085 last week.

- Canada and Alberta have agreed to advance a new major oil pipeline, backed by more than C$150 billion in related infrastructure investments, as part of a broader strategy to diversify energy exports beyond the U.S. The project would transport approximately 1 million barrels per day along a southern route, while preserving B.C.'s northern oil tanker ban, expanding port and LNG infrastructure, reducing methane emissions, and providing a meaningful Indigenous ownership stake. By retaining key environmental safeguards and beginning consultations immediately, governments aim to reduce regulatory and legal risks that have delayed previous pipeline projects, though the project continues to face criticism over costs and climate impacts.

- The Greater Toronto Area housing market continued to strengthen in June, with home sales rising 9.4% year-over-year to 6,770 while new listings fell 12.9% to 17,282, tightening market conditions after a slow start to the year. Although the average selling price remained 3.9% below last year ($1.06 million) and the MLS Home Price Index was down 5.4%, both prices and sales improved on a seasonally adjusted month-over-month basis. With first-half sales edging above 2025 levels and inventory tightening, TRREB expects stronger buyer competition and a return to price growth in the second half of 2026, supported by pent-up demand.

- U.S. job growth slowed in June, with nonfarm payrolls rising 57,000, below expectations, while downward revisions to April and May left net employment down 17,000 over the three-month period. Despite the softer headline, the labour market remains stronger than in 2025, averaging 92,000 new jobs per month in the first half of 2026 versus 10,000 per month last year. The 4.2% unemployment rate declined largely because fewer people participated in the labour force, while hiring remained concentrated in health care and professional services. Wage growth stayed steady at 3.5% year-over-year, and low jobless claims suggest the labour market continues to expand, albeit at a more moderate pace.

- The U.S. is launching "Trump Accounts" on July 4, introducing tax-advantaged investment accounts for children under 18 designed to encourage long-term wealth creation. Starting with eligible children born between 2025 and 2028 receive a one-time $1,000 federal contribution, with families able to contribute up to $5,000 annually. Funds are invested in U.S. equity index funds and generally remain inaccessible until age 18, reflecting a policy shift toward expanding household participation in long-term equity ownership and retirement savings.

- Central banks continue to drive structural demand for gold, with a record 90% citing its performance during financial crises as a key reason for holding the metal, while 84% view it as a long-term inflation hedge and 85% of emerging-market central banks see it as protection against geopolitical risk. Central banks have purchased roughly 1,000 tonnes of gold annually over the past four years—double the pace of the previous decade—highlighting gold’s growing role in reserve diversification. While higher real interest rates may weigh on prices in the near term, continued official-sector buying is widely viewed as an important long-term support for the gold market.

Weekly Diversion:

Check out this video: I know it's Stampede, but here's 2 minutes of the best Group Stage Goals

Charts of the Week

Nuclear energy is becoming a more important part of the global energy conversation. Unlike fossil fuels, nuclear plants can provide large volumes of reliable, around-the-clock electricity with very low operating emissions. That makes the sector increasingly relevant as electricity demand rises from data centers, electrification, manufacturing, and AI-related infrastructure.

One of the more important takeaways is the age of the existing global reactor fleet. A large share of operating reactors is now approaching or has exceeded several decades of service. The first chart shows a meaningful concentration of reactors around the 35-to-45-year range, highlighting the need for life extensions, refurbishment, replacements, and new capacity over time. While aging facilities can remain operational with investment and regulatory approval, the broader trend reinforces the importance of continued nuclear development rather than relying solely on the current fleet.

Source: First Trust Advisors

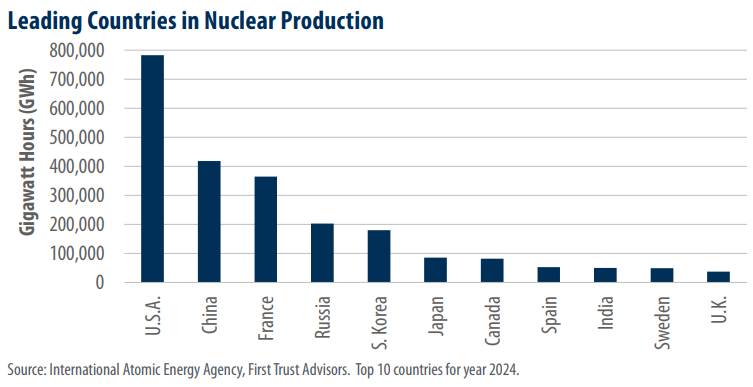

The United States remains the largest producer of nuclear electricity as the next chart illustrates, generating roughly 781,000 gigawatt hours in 2024. China ranks second, but its growth trajectory may be more important than its current position: it has dozens of reactors under construction and significant plans to expand capacity further. That expansion matters because nuclear power requires a dependable long-term supply of uranium, creating a structural link between rising reactor capacity and uranium demand.

Source: First Trust Advisors

Source: First Trust Advisors

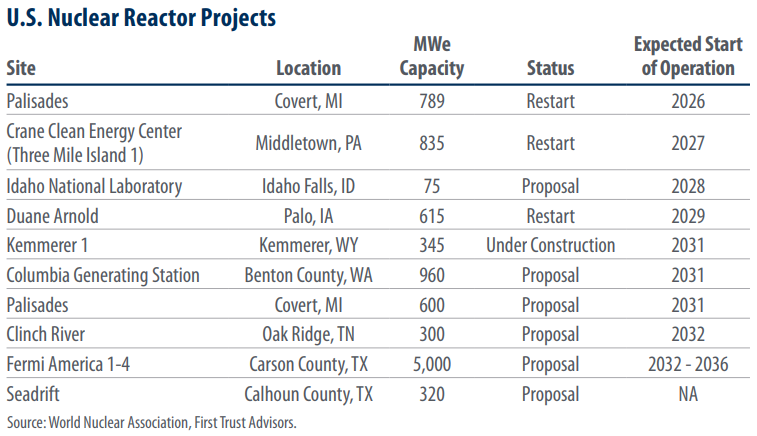

The U.S. is also now showing renewed interest in nuclear capacity through reactor restarts, plant life extensions, and proposed new projects. Although new nuclear development can take years and face high costs and regulatory hurdles, recent activity in the last table below suggests that policymakers and utilities are increasingly focused on energy reliability and grid capacity alongside emissions reduction.

Source: First Trust Advisors

Source: First Trust Advisors

For our investors, this is part of the long-term backdrop supporting uranium demand. New reactors, reactor restarts, and the need to replace aging capacity can all increase future uranium requirements, while supply takes time to develop. This theme is one reason we maintain a meaningful exposure to the Sprott Physical Uranium Trust as part of our Real Assets allocation, which offers direct exposure to the physical uranium market. As with any commodity-related holding, uranium prices can be volatile at times, but the longer-term supply-demand outlook continues to be supported by the global push for reliable, low-carbon electricity generation.

Sources: Yahoo Finance, First Trust, The Guardian, Toronto Regional Real Estate Board, CNBC, First Trust Economics, International Atomic Energy Agency, World Nuclear Association

©2026 Milestone Wealth Management Ltd. All rights reserved.

DISCLAIMER: Investing in equities is not guaranteed, values change frequently, and past results are not necessarily an indicator of future performance. Investors cannot invest directly in an index. Index returns do not reflect any fees, expenses, or sales charges. Opinions and estimates are written as of the date of this report and may change without notice. Any commentaries, reports or other content are provided for your information only and are not considered investment advice. Readers should not act on this information without first consulting Milestone, their investment advisor, tax advisor, financial planner, or lawyer. This communication is intended for Canadian residents only and does not constitute as an offer or solicitation by anyone in any jurisdiction in which such an offer is not allowed.