Market Insights: Pause, Not Breakdown: What the Charts Are Telling Us?

Milestone Wealth Management Ltd. - Jun 19, 2026

Macroeconomic and Market Developments:

- North American markets were mixed this week. In Canada, the S&P/TSX Composite Index declined by -0.23%, while in the U.S., the Dow Jones Industrial Average increased by 1.41% and the S&P 500 Index rose by 1.44%.

- The Canadian Dollar weakened again this week, closing at 70.56 vs. 71.50 cents USD last week.

- Oil prices dropped this week, with U.S. West Texas Crude closing at US$76.54 vs. US$84.29 last week.

- The price of Gold fell this week closing at US$4,173 vs. US$4,235 last week.

- Canadian economic data was mixed this week, but still useful for gauging momentum. The most constructive release came from manufacturing, where April sales rose 4.2% to a record C$77.1 billion, following a 3.4% gain in March. Strength was led by petroleum and coal products, up 22.6%, and food, up 2.9%, though sales were still up 1.4% excluding petroleum and coal. Retail sales were more moderate, rising 0.5% in April, while volumes were flat and core retail sales fell 0.7% for the second straight month. Overall, the data points to an economy with strength in goods production, but softer underlying momentum from consumers.

- U.S. retail sales rose 0.9% in May, beating expectations and reinforcing the resilience of the U.S. consumer, with sales up 6.9% from a year earlier. The gain was broad-based, led by gasoline stations, online retailers, and autos, while core retail sales, which exclude autos, building materials, and gas, rose 0.6%. Although the report supports the view that consumer spending remains a source of strength for the economy, some caution is warranted, as the figures are not adjusted for inflation and restaurant and bar sales declined for the first time in four months, suggesting higher energy costs may be starting to weigh on discretionary spending.

- The Federal Reserve held rates steady at 3.5% to 3.75% this week, but the bigger story was the first meeting under Kevin Warsh, the newly appointed Fed Chair and former Fed Governor. It was the Fed’s fourth straight hold, but 9 of 18 officials now expect at least one rate hike by year-end. Warsh also removed forward guidance and launched five task forces to review Fed communications, inflation, jobs, productivity, and economic data. For markets, the takeaway is a Fed that may be less predictable, more data-dependent, and still focused on inflation before moving toward rate cuts.

- Oil prices fell sharply this week after the U.S.-Iran interim deal improved the outlook for the Strait of Hormuz, with Brent and WTI dropping back toward pre-war levels; even so, the physical market is not fully loose yet, as U.S. crude inventories fell another 8.3 million barrels and remain below seasonal norms, meaning the geopolitical premium has faded faster than the underlying tightness.

Weekly Diversion:

Check out this video: The Business Behind the Players We Watch

Charts of the Week

With so much noise in the market, it is easy to overreact to every red or green day. One weak session can make investors worry that a new downturn is beginning, while one strong session can quickly bring back calls for new highs.

The bigger picture is more balanced. After a strong rally off the March lows, the S&P 500 Index has been trading in a relatively tight range of roughly 5%. This type of consolidation is normal after a sharp recovery move higher. It allows the market to work through short-term uncertainty before choosing its next direction.

The first chart shows that the index has not broken down, but it has also not clearly broken out. Until that range is resolved, investors should expect more back-and-forth price action.

Source: The Chart Report, Trading View

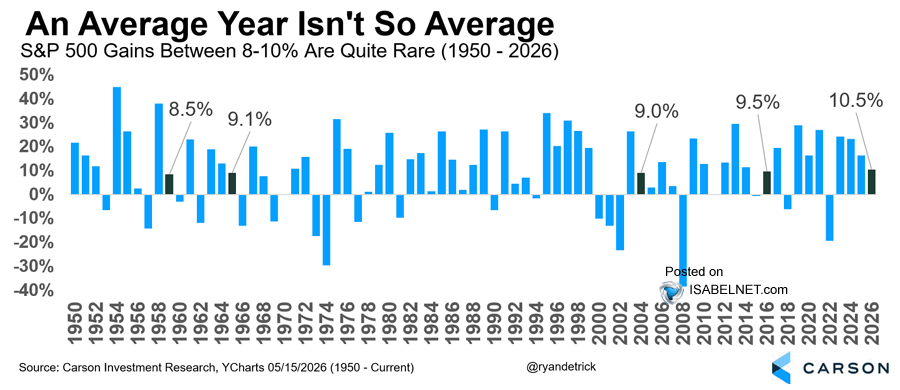

The next chart adds useful historical context. Since 1950, the S&P 500 has rarely delivered returns that are close to average. Most years finish either meaningfully above or below the long-term average. That matters today because a mid-year pause does not necessarily mean the rally has run its course.

Source: Carson Investment Research, @ryandetrick, ISABELNET

After a strong second quarter, some consolidation is normal. However, history shows that markets often move more than investors expect, in either direction. For now, the S&P 500 remains in a constructive trend, but the next major move likely depends on whether the index can break out of its current trading range.

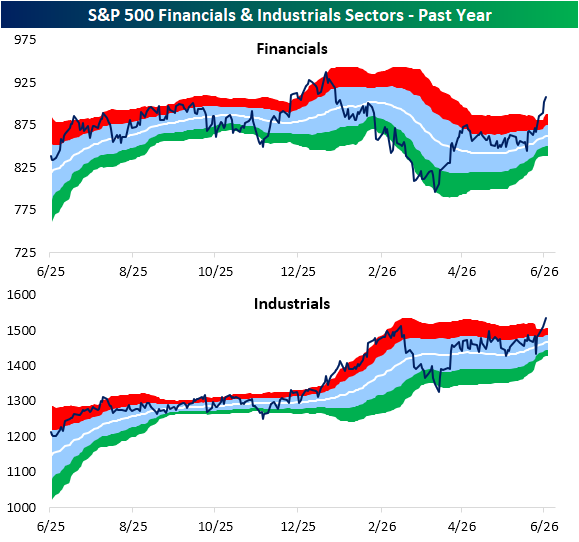

The final chart looks beneath the surface of the S&P 500. While Technology and AI continue to get most of the headlines and attention, Financials and Industrials have also started to show some strength. Industrials have broken out to new 52-week highs, while Financials have moved above recent lower highs.

Source: Bespoke

That is important because broader participation outside of Technology would make the market’s advance healthier. A market led by only a small group of large cap Tech stocks is more vulnerable. A market where cyclical sectors like Financials and Industrials are also improving is more balanced.

Overall, the charts point to a market that is pausing, not necessarily breaking down. The S&P 500 still needs a clear breakout from its current range, but improving sector participation suggests the underlying trend remains positive.

Sources: Reuters, National Bank Financial, Bank of Canada, First Trust Data Watch, Bureau of Labor Statistics, @Ryan Detrick, StockCharts, The Chart Report, TradingView

©2026 Milestone Wealth Management Ltd. All rights reserved.

DISCLAIMER: Investing in equities is not guaranteed, values change frequently, and past results are not necessarily an indicator of future performance. Investors cannot invest directly in an index. Index returns do not reflect any fees, expenses, or sales charges. Opinions and estimates are written as of the date of this report and may change without notice. Any commentaries, reports or other content are provided for your information only and are not considered investment advice. Readers should not act on this information without first consulting Milestone, their investment advisor, tax advisor, financial planner, or lawyer. This communication is intended for Canadian residents only and does not constitute as an offer or solicitation by anyone in any jurisdiction in which such an offer is not allowed.