Market Insights: Momentum with Potential Room to Run

Milestone Wealth Management Ltd. - May 08, 2026

Macroeconomic and Market Developments:

- North American markets were up this week. In Canada, the S&P/TSX Composite Index closed 0.55% higher, while in the U.S., the Dow Jones Industrial Average inched ahead by 0.22% and the S&P 500 Index jumped 2.33% driven by tech-heavy performance.

- The Canadian Dollar fell this week, closing at 73.08 vs. 73.54 cents USD last week.

- Oil prices decreased this week, with U.S. West Texas Crude closing at US$94.87 vs. US$102.11 last week.

- The price of Gold rose this week closing at US$4,725 vs. US$4,621 last week.

- The U.S. economy added 115,000 jobs in April, comfortably above expectations for 62,000, while the unemployment rate held steady at 4.3%, suggesting the labor market remains resilient despite geopolitical uncertainty and slowing areas of the economy; gains were led by healthcare, transportation, retail, and social assistance, while manufacturing and government employment declined, and although the report likely reduces the urgency for near-term rate cuts, economists noted the data was not strong enough to materially increase expectations for additional tightening by the Federal Reserve.

- The U.S. trade deficit narrowed slightly to $60.3B in March, as exports rose $6.2B—driven largely by crude oil and petroleum products amid disruptions tied to the Strait of Hormuz conflict—while imports increased $8.7B, led by autos and technology-related goods; economists Brian S. Wesbury and Robert Stein noted that although overall trade volumes remain relatively flat year-over-year, the composition has improved for domestic producers, with exports up 13.3% and imports down 9.0%, while shifting global supply chains continue to reshape trade flows, including a sharp decline in Chinese exports to the U.S. and a surge in AI-related imports from Taiwan.

- Canada’s labour market weakened in April, with the economy unexpectedly losing 18,000 jobs while the unemployment rate rose to 6.9%, highlighting continued softness in hiring amid trade uncertainty and slowing economic momentum; although economists noted the increase in unemployment was driven more by workers voluntarily leaving jobs than permanent layoffs, Canada has now lost 112,000 jobs since January, primarily in manufacturing and wholesale trade.

- Momentum is building behind a major new Canada-U.S. oil pipeline project proposed by South Bow and Bridger Pipeline, with sources indicating producers have already committed roughly 400,000 bpd (~72% of initial capacity) toward the planned 550,000 bpd Alberta-to-Wyoming pipeline, bringing the project close to the threshold typically required to proceed; backed by support from President Donald Trump and major Canadian producers including Cenovus Energy and Canadian Natural Resources, the project highlights ongoing demand for additional export capacity as Canadian crude production continues to grow, reinforcing broader expectations for expanded North American energy infrastructure and cross-border energy integration through the end of the decade.

- Anthropic has reportedly signed a $1.8B, seven-year computing agreement with Akamai Technologies to support rapidly growing demand for its AI models, underscoring the intensifying race for compute infrastructure across the AI industry; Anthropic’s CEO noted the company experienced ~80x growth in annualized revenue and usage in Q1, while the deal—Akamai’s largest ever—highlights how cloud providers, chip suppliers, and infrastructure firms are increasingly positioning themselves to capitalize on the accelerating adoption of enterprise AI tools.

Weekly Diversion:

Check out this video: I wonder what Calgary will do for the Hockey World Cup

Charts of the Week

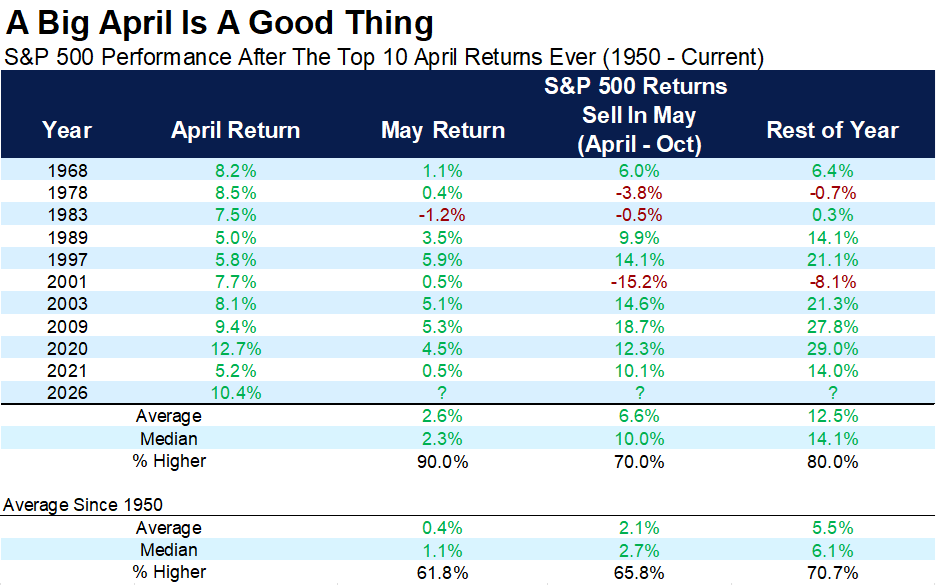

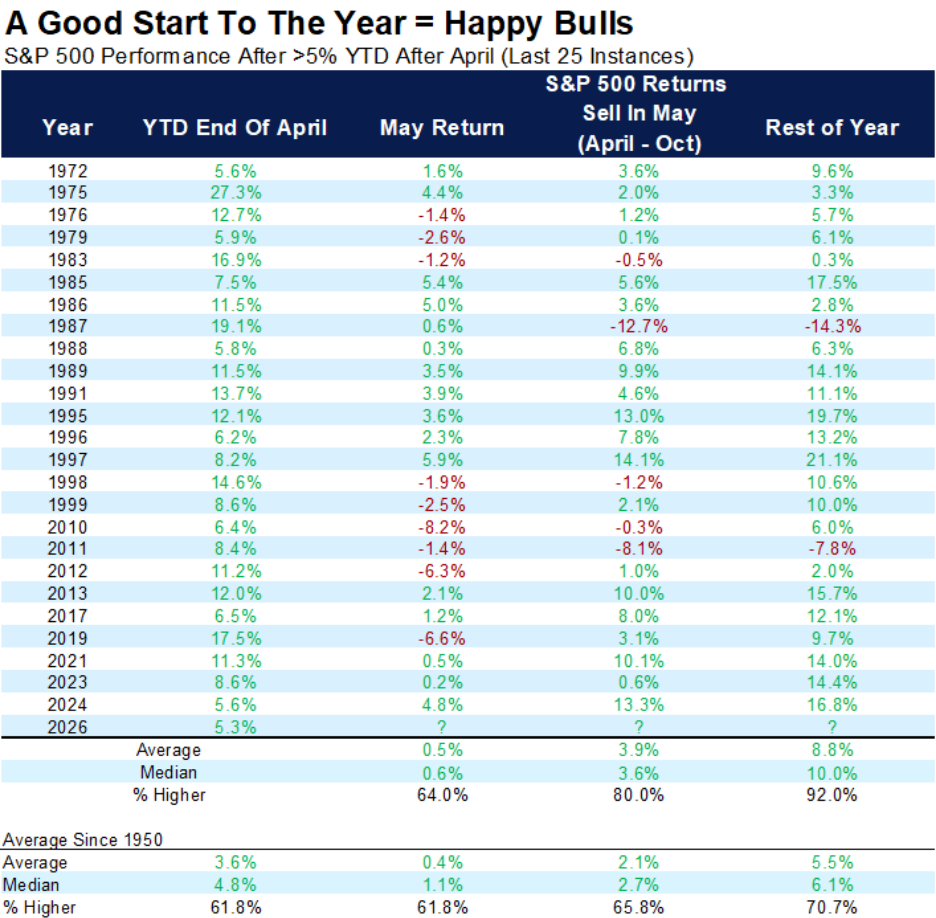

History shows that strong gains rarely stand alone. When markets rally early in the year or in the first few years of a cycle, they have often signaled further upside, not necessarily an imminent peak. The tables and charts that follow illustrate how robust April returns, solid year‑to‑date performance, and milestones like a market doubling from its lows have historically preceded continued advances, suggesting today’s bull market may still have room to run, albeit likely with some caution.

The first table shows that exceptionally strong April returns have historically been followed by favorable outcomes in both May and the remainder of the year, with the index advancing in May in nine of the top ten instances and the rest‑of‑year return averaging well into the double digits. The second table looks at years when the market was already up more than 5% by the end of April and finds that, in 23 of the past 25 such cases, prices continued to rise over the balance of the year, reinforcing the idea that upside momentum tends to persist longer than expected rather than abruptly reverse.

Source: Carson Investment Research, FactSet, @ryandetrick

Source: Carson Investment Research, FactSet, @ryandetrick

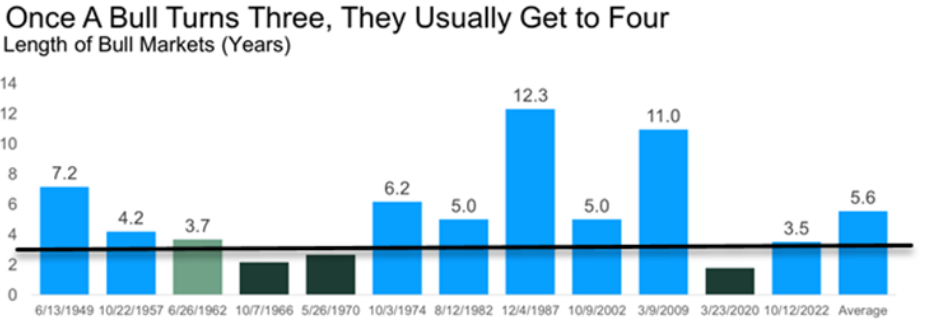

The following bar chart on bull market longevity highlights that, once advances have survived to their third anniversary, they have almost always extended to a fourth, and the last five such cycles that reached age three went on to last an average of roughly eight years, with even the shortest stretching to about five. This historical context suggests that a three-and-a-half-year-old advance should be viewed as middle‑aged rather than elderly, leaving potential room for further advance.

Source: Carson Investment Research, FactSet, @ryandetrick

Source: Carson Investment Research, FactSet, @ryandetrick

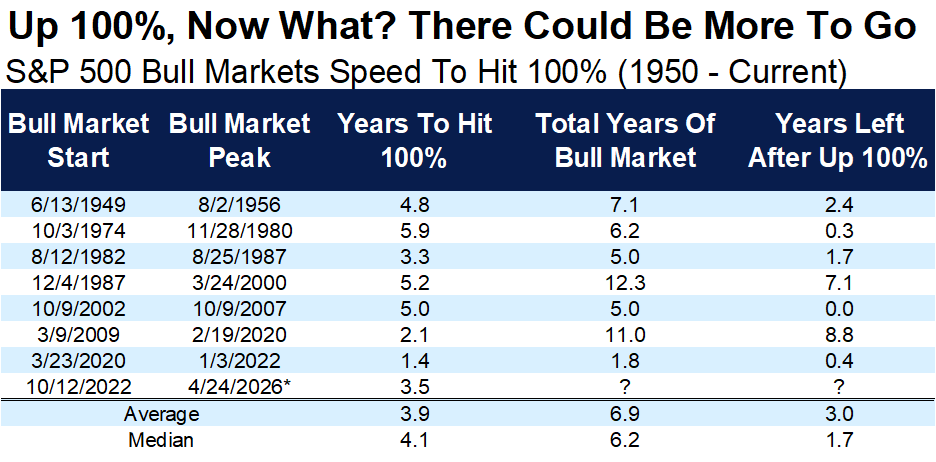

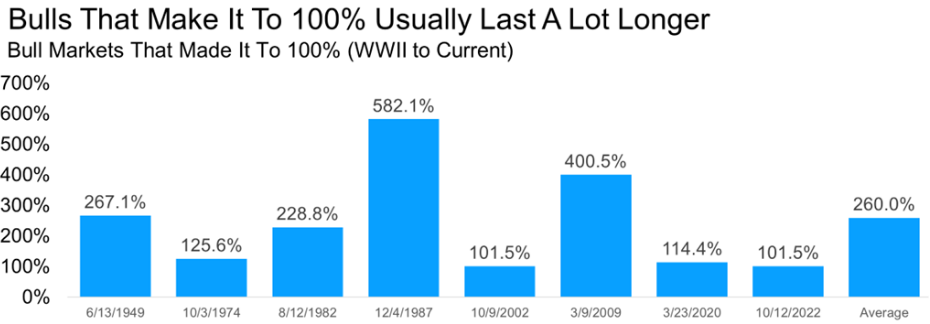

The following table and chart deepen this argument by examining prior instances when the index had doubled from a major low. Across seven such episodes, the market took about four years on average to reach the 100% mark, yet those bull markets continued for roughly three additional years after that milestone and as shown in the second chart, ultimately delivered total gains of around 260%, far beyond the initial doubling.

Source: Carson Investment Research, FactSet, @ryandetrick

Source: Carson Investment Research, FactSet, @ryandetrick

Sources: Yahoo Finance, The Canadian Press, BOE, Fox Business, Bloomberg, First Trust, Carson Investment Research, FactSet, @ryandetrick, YCharts

©2026 Milestone Wealth Management Ltd. All rights reserved.

DISCLAIMER: Investing in equities is not guaranteed, values change frequently, and past results are not necessarily an indicator of future performance. Investors cannot invest directly in an index. Index returns do not reflect any fees, expenses, or sales charges. Opinions and estimates are written as of the date of this report and may change without notice. Any commentaries, reports or other content are provided for your information only and are not considered investment advice. Readers should not act on this information without first consulting Milestone, their investment advisor, tax advisor, financial planner, or lawyer. This communication is intended for Canadian residents only and does not constitute as an offer or solicitation by anyone in any jurisdiction in which such an offer is not allowed.