Market Insights: Broadening Earnings Upswing

Milestone Wealth Management Ltd. - Apr 24, 2026

Macroeconomic and Market Developments:

- North American markets were mixed this week. In Canada, the S&P/TSX Composite Index closed 1.29% lower, while in the U.S., the Dow Jones Industrial Average decreased by 0.44% and the S&P 500 Index rose 0.55%.

- The Canadian Dollar rose slightly this week, closing at 73.18 vs. 73.01 cents USD last week.

- Oil prices jumped this week, with U.S. West Texas Crude closing at US$94.75 vs. US$83.00 last week.

- The price of Gold fell this week closing at US$4,730 vs. US$4,861 last week.

- U.S. retail sales surged 1.7% in March (4.0% y/y), beating expectations, marking the strongest monthly gain in a year, driven in large part by a 15.5% spike in gas station sales amid higher energy prices, though underlying momentum remained more moderate with “core” sales up 0.6%; economists Brian S. Wesbury and Robert Stein note that while consumer spending appears resilient on the surface—with solid gains across most categories—the inflation-adjusted picture remains weak, with real retail sales up just 0.7% over the past year and still below 2022 levels, highlighting a consumer backdrop that is holding up but not accelerating meaningfully amid ongoing geopolitical and price pressures.

- Kevin Warsh signaled a potential shift in how the Federal Reserve measures inflation, advocating for greater use of “trimmed” metrics (excluding outliers) rather than relying primarily on traditional gauges like PCE, arguing these measures show inflation trends as more moderate (e.g., ~2.3%–2.8%); while the proposal could influence future rate decisions and support a more dovish policy stance, critics warn it may introduce bias or appear as “goalpost shifting,” highlighting the potential for market sensitivity to any changes in how inflation is interpreted and communicated.

- Canadian retail sales rose 0.7% m/m to CAD $72.1B in February, slightly missing expectations but showing broad-based strength across 7 of 9 subsectors, led by a 1.0% gain in motor vehicle sales, while core retail sales (ex-autos and fuel) increased 0.6%, indicating underlying resilience; preliminary estimates point to another +0.6% increase in March, suggesting steady—though not accelerating—consumer momentum amid a still-mixed economic backdrop.

- Enbridge received federal approval for a $4B expansion of its Westcoast natural gas pipeline in British Columbia, adding ~300 MMcf/d of capacity to support growing LNG exports and domestic demand, with construction expected to begin this summer and completion targeted for 2028; the project—fully subscribed and backed by industry demand—signals a more supportive federal stance toward energy infrastructure under Mark Carney, though it continues to face criticism from environmental groups, highlighting the ongoing tension between energy security, economic growth, and climate policy in Canada.

- Starbucks is expanding operations in Tennessee with a $100M investment and ~2,000 new jobs, potentially costing Seattle up to $750M in future tax revenue as growth shifts away from its home base, highlighting how corporate location decisions are increasingly influenced by regional tax and regulatory environments; the move comes amid declining business climate rankings in Washington and the introduction of a new high-income tax, underscoring broader concerns around capital migration and economic competitiveness at the state level.

Weekly Diversion:

Check out this video: That settles it, I’m buying one this weekend

Charts of the Week

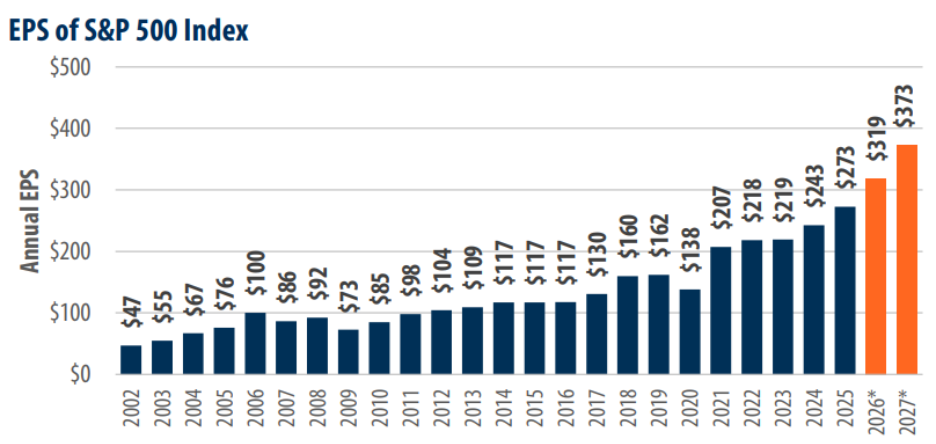

Earnings per share (EPS) for a broad equity index offers a concise way to track the health and trajectory of corporate profits, and the accompanying charts paint a picture of both resilience and renewed momentum in the current cycle. Taken together, they show a market that has absorbed a severe shock, moved into a powerful recovery phase, and is now transitioning into a period of broad-based, though uneven, profit growth across sectors.

The long‑term EPS line rises from modest levels in the early 2000s, dips around major crises, and then falls sharply during the pandemic before snapping back to new highs in the mid‑2020s. Recent and projected figures climb from the mid‑200s into the low‑300s and then the high‑300s over two years, implying back‑to‑back growth rates in the high teens—among the steepest slopes on the chart. This visual captures how earnings not only recovered but are expected to push into an unusually strong expansion.

Source: Capital IQ, First Trust Advisors

Source: Capital IQ, First Trust Advisors

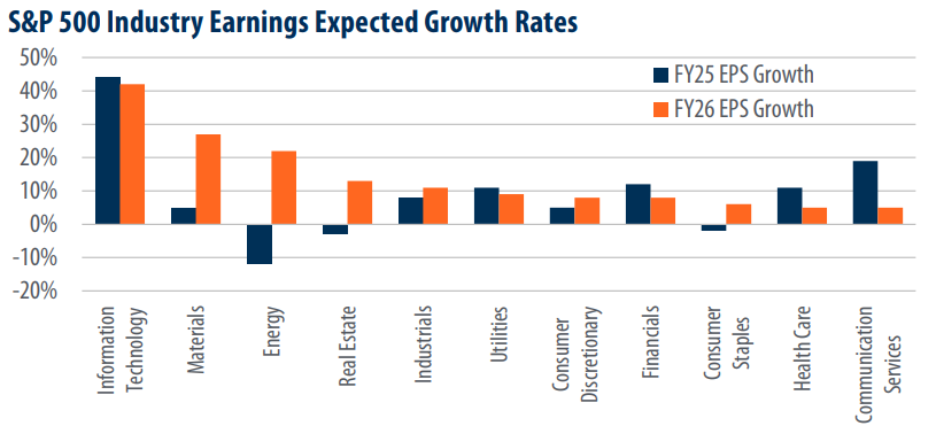

The sector growth bar chart adds nuance by revealing how uneven that expansion is. Every major industry is projected to grow, but the side‑by‑side bars show that energy shifts from a double‑digit decline to more than 20% growth, and materials leap from low single‑digits to the high‑20s. By contrast, communication services slow from high teens growth to mid‑single digits, with financials and health care also cooling, hinting at a rotation in leadership towards cyclicals rather than uniform strength.

Source: Bloomberg, First Trust Advisors

Source: Bloomberg, First Trust Advisors

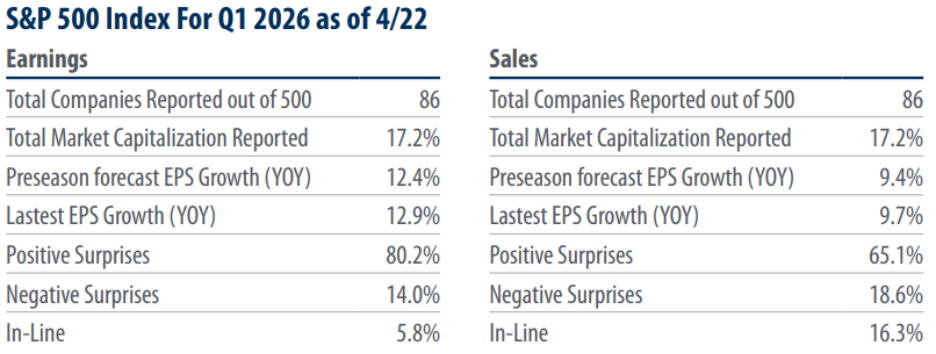

Finally, the early season earnings table for the first quarter of 2026 offers a real‑time check on these themes. With only 86 companies reporting as of 4/22, representing just over 17% of the index’s value, earnings growth of 12.9% is already slightly ahead of preseason expectations, and nearly four‑fifths of results are positive surprises, with similar outperformance in revenue. Even at this early stage, actual numbers are aligning with—and modestly surpassing—the robust growth trajectory implied by the charts. Next week should provide much more evidence, as the Mag-7 stocks (Nvidia, Apple, Microsoft, etc) all report next week, and they make up approximately one-third of the index.

Source: Bloomberg, First Trust Advisors

Source: Bloomberg, First Trust Advisors

The current earnings cycle appears firmly in expansion mode, with profits not only recovering but pushing toward some of the fastest projected growth in years. Sector leadership is rotating toward areas like energy and materials, while early 2026 earnings results—already ahead of expectations—reinforce a still-supportive backdrop for equities where sector selectivity is likely to be rewarded. However, with inflation currently accelerating and central bank interest cuts on hold for now, the upside could be limited if this pace of earnings growth doesn’t continue.

Sources: Yahoo Finance, The Canadian Press, Action Forex, Fox Business, BNN, Richardson Wealth, Capital IQ, First Trust Advisors, Bloomberg

©2026 Milestone Wealth Management Ltd. All rights reserved.

DISCLAIMER: Investing in equities is not guaranteed, values change frequently, and past results are not necessarily an indicator of future performance. Investors cannot invest directly in an index. Index returns do not reflect any fees, expenses, or sales charges. Opinions and estimates are written as of the date of this report and may change without notice. Any commentaries, reports or other content are provided for your information only and are not considered investment advice. Readers should not act on this information without first consulting Milestone, their investment advisor, tax advisor, financial planner, or lawyer. This communication is intended for Canadian residents only and does not constitute as an offer or solicitation by anyone in any jurisdiction in which such an offer is not allowed.