Market Insights: Nasdaq Rallies and Future Returns

Milestone Wealth Management Ltd. - Apr 10, 2026

Macroeconomic and Market Developments:

- North American markets were up over the last two weeks. In Canada, the S&P/TSX Composite Index closed 5.43% higher, while in the U.S., the Dow Jones Industrial Average increased by 6.09% and the S&P 500 Index jumped 7.04%.

- The Canadian Dollar was stagnant over the last two weeks, closing at 72.26 vs. 72.19 cents USD two weeks ago.

- Oil prices fell over the last two weeks, with U.S. West Texas Crude closing at US$95.83 vs. US$99.64 two weeks ago.

- The price of Gold rose over the last two weeks closing at US$4,769 vs. US$4,492 two weeks ago.

- U.S. inflation surprised to the upside in March, with the CPI rising 0.9% m/m and 3.3% y/y, driven largely by a 10.9% surge in energy prices (gasoline +21.2%), while core CPI rose a more modest 0.2% m/m (2.6% y/y)—suggesting underlying inflation pressures remain elevated but more contained; notably, real wages declined 0.6% on the month, highlighting ongoing pressure on consumers, while economists Brian S. Wesbury and Robert Stein point to energy-driven volatility and still-sticky housing costs as key uncertainties, leaving the Federal Reserve with limited conviction to adjust rates in the near term despite inflation remaining above its 2% target.

- U.S. retail sales rose 0.6% in February (3.7% y/y), beating expectations, driven by gains in autos, gas, and online spending, though underlying momentum remains softer with “core” sales up 0.4% and real (inflation-adjusted) sales down at a 0.7% annualized pace over the past six months, suggesting consumers are still under pressure; economists Brian S. Wesbury and Robert Stein note much of the strength reflects a rebound from weather-related weakness in January, while pointing to moderating consumption trends and mixed signals across employment and money supply data, reinforcing a cautiously slowing—but still resilient—consumer backdrop.

- Canada’s labour market showed modest stabilization in March, with +14.1K jobs added following earlier losses, while the unemployment rate held at 6.7%, as gains in services and natural resources were offset by continued weakness in trade-sensitive sectors; wage growth remained strong (+5.1% y/y)—a potential inflation concern—while regional disparities persisted, and with these mixed signals, the Bank of Canada has kept rates on hold for now but is facing increasing pressure around potential rate hikes later this year.

- Mark Carney moved to the brink of a majority government after Marilyn Gladu defected from the Conservatives to the Liberals, bringing the party to 171 seats—just one shy of a majority in the House of Commons, marking the fifth defection in recent months and underscoring shifting political dynamics amid economic uncertainty; however, Pierre Poilievre criticized the move as undermining voter intent, highlighting growing political tension as the Liberals edge closer to consolidating power without a formal election.

- CoreWeave shares surged ~13% after announcing a multi-year agreement with Anthropic to provide large-scale compute infrastructure for AI model training and deployment, reinforcing intensifying demand for high-performance chips amid the ongoing AI buildout; the deal adds to a broader industry trend where major players—including Broadcom, Google, and Meta—are investing heavily in custom semiconductors and securing long-term compute capacity, highlighting the escalating “arms race” for AI infrastructure as companies seek to mitigate chip shortages and scale next-generation AI systems.

- Meta faces increasing legal pressure after the Massachusetts Supreme Judicial Court ruled the company must proceed to trial in a lawsuit alleging its Instagram platform was deliberately designed to addict children, marking a key development as the court found claims targeting platform design and corporate conduct—rather than user-generated content—are not shielded by Section 230; the decision adds to a growing wave of litigation across the U.S., including recent jury rulings and state-led cases, highlighting rising regulatory and legal risks for social media firms as scrutiny intensifies around youth safety, platform design, and accountability.

Weekly Diversion:

Check out this video: In honor of the Masters, here are Rory McIlroy’s best shots from the 2025 Masters

Charts of the Week

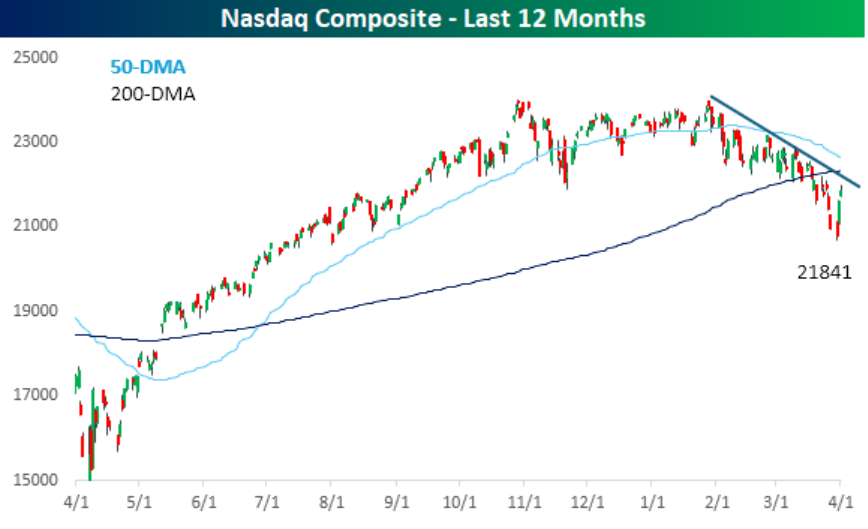

Last week’s action in the Nasdaq offered a sharp, but still tentative, countertrend move within an established downswing. The 12-month price chart shows a clear pattern of lower highs and lower lows, and even with the latest two-day surge, the index remains below its declining 50- and 200-day moving averages, reinforcing that the primary trend is still downward rather than decisively reversed.

Source: Bespoke Investment Group

Source: Bespoke Investment Group

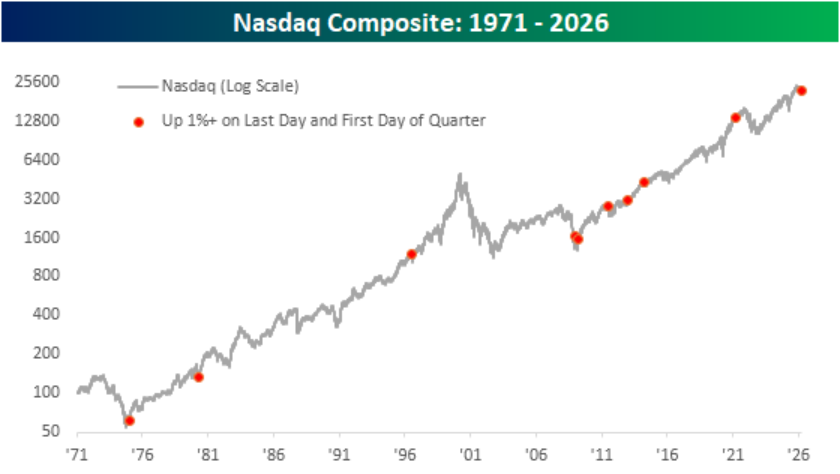

Looking at a longer-term perspective, the recent two-day pattern is notably rare. Since the early 1970s, there have only been ten instances where the Nasdaq gained at least 1% on both the final trading day of a quarter and the first trading day of the next. Historically, these occurrences have tended to cluster around intermediate bottoms or mid-cycle pauses, rather than at the beginning of major bear markets. This suggests that such patterns have more often reflected underlying resilience in growth equities, rather than signaling further deterioration.

Source: Bespoke Investment Group

Source: Bespoke Investment Group

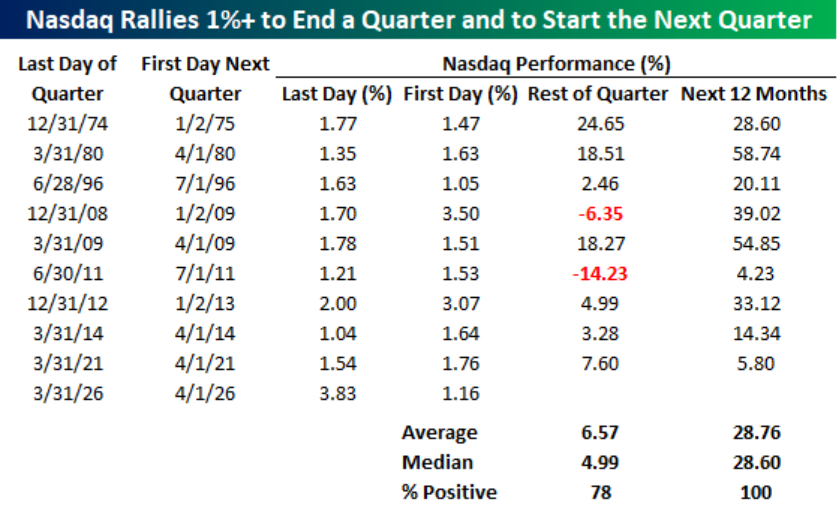

Forward return data further reinforces this view. Following similar setups, the Nasdaq has historically delivered an average gain of 6.6% over the remainder of the quarter, with positive returns roughly 75% of the time. Over a longer horizon, the results are even more compelling—average 12-month returns of approximately 28.8%, with gains observed in every historical instance. While past performance is not indicative of future results, the consistency of these outcomes highlights a strong historical tailwind following such signals.

Source: Bespoke Investment Group

Source: Bespoke Investment Group

That said, the path forward has not always been smooth. In several instances—particularly around periods such as 2008–2009 and 2011—short-term returns were negative despite strong longer-term gains. This serves as an important reminder that volatility can persist even within a constructive forward return environment.

From a portfolio positioning standpoint, last week’s pattern should not be interpreted as a signal to disregard near-term risks. Rather, it suggests that while the current downtrend may continue to generate short-term uncertainty, the historical probability has favored investors who maintained or incrementally increased exposure over the subsequent quarter and year.

Sources: Yahoo Finance, Reuters, First Trust, BBC, Richardson Wealth, Bespoke Investment Group

©2026 Milestone Wealth Management Ltd. All rights reserved.

DISCLAIMER: Investing in equities is not guaranteed, values change frequently, and past results are not necessarily an indicator of future performance. Investors cannot invest directly in an index. Index returns do not reflect any fees, expenses, or sales charges. Opinions and estimates are written as of the date of this report and may change without notice. Any commentaries, reports or other content are provided for your information only and are not considered investment advice. Readers should not act on this information without first consulting Milestone, their investment advisor, tax advisor, financial planner, or lawyer. This communication is intended for Canadian residents only and does not constitute as an offer or solicitation by anyone in any jurisdiction in which such an offer is not allowed.