Market Insights: Why Inflation Has Put Real Assets Back in Focus

Milestone Wealth Management Ltd. - Mar 06, 2026

Macroeconomic and Market Developments:

- North American markets were down sharply this week. In Canada, the S&P/TSX Composite Index closed 3.66% lower, while in the U.S., the Dow Jones Industrial Average fell by 3.01% and the S&P 500 Index declined 2.02%.

- The Canadian Dollar inched up again this week, closing at 73.65 vs. 73.23 cents USD last week.

- Oil prices spiked 35% this week, with U.S. West Texas Crude closing at US$90.90 vs. US$67.29 last week. This 35% increase is the largest weekly jump ever going back to at least the early 1980s.

- The price of Gold came down this week closing at US$5,161 vs. US$5,281 last week.

- U.S. retail sales slipped 0.2% in January, slightly better than expectations for a 0.3% decline, largely reflecting severe winter weather that disrupted consumer activity across much of the country. Weakness was concentrated in gas stations (-2.9%), health & personal care stores (-3.0%) and auto sales (-0.9%), while online and non-store retailers rose 1.9% as consumers shifted spending online during the storms. Core retail sales — which exclude autos, gas and building materials and are closely watched for GDP — rose 0.2%, suggesting underlying demand remains stable, though inflation-adjusted retail sales have risen just 0.7% over the past year and remain below their 2022 peak, pointing to a broader trend of soft consumer spending.

- U.S. manufacturing activity remained in expansion territory in February, with the ISM Manufacturing Index at 52.4 (above the 50-expansion threshold and ahead of the 51.5 consensus), marking a second consecutive month of growth. New orders (55.8) and production (53.5) stayed firmly positive, while the employment index improved to 48.8 but remained in contraction. However, inflation pressures resurfaced as the prices paid index surged to 70.5 from 59.0, signaling persistent cost pressures even as broader manufacturing demand shows signs of stabilizing.

- U.S. nonfarm payrolls fell by 92,000 in February, well below expectations for a +55,000 gain, while December and January payrolls were revised down by a combined 69,000, bringing the total net decline to 161,000. The weakness was concentrated in leisure & hospitality (-27K), healthcare (-18.6K), education (-15.7K) and manufacturing (-12K). Economists caution the report may overstate underlying weakness, noting January’s strong job gains and temporary disruptions — including severe winter storms and healthcare strike activity — likely weighed on February hiring. In addition, changes in U.S. immigration policy have reduced labour supply, contributing to slower job growth. While hiring momentum has cooled, analysts emphasize the data does not currently signal recession, with productivity growth and steady wage gains helping support continued economic expansion.

- Lloyd's of London is in discussions with the U.S. International Development Finance Corporation to provide political risk insurance and guarantees for vessels operating in the Gulf, as escalating geopolitical tensions threaten maritime trade through the Strait of Hormuz, a corridor that carries roughly 20% of global oil supplies. About 1,000 vessels with an estimated $25B in hull value — roughly half oil and gas tankers — remain in Gulf waters, prompting insurers to expand high-risk zones and raising war-risk premiums. The initiative highlights growing coordination between governments and insurers to maintain energy supply chains and stabilize global shipping markets during periods of heightened geopolitical risk.

- Chevron Corporation warned that proposed emissions rules under California’s “cap-and-invest” program could threaten the viability of the state’s remaining refineries, potentially driving fuel prices up by more than $1 per gallon and putting over 500,000 energy-sector jobs at risk. In a letter to Gavin Newsom, company executives argued that tightening carbon caps and removing emissions allowances could accelerate refinery closures, reduce West Coast fuel supply resilience, and raise affordability concerns for consumers, while regulators say the policy is aimed at meeting the state’s aggressive emissions reduction targets.

- Canadian Natural Resources Ltd. has deferred early engineering work on its proposed $8.25B Jackpine oilsands expansion, citing regulatory uncertainty around carbon pricing and methane rules as Ottawa finalizes new environmental policies. The company had planned to spend about $150M in 2026 on early project work but is pausing until clearer policy direction emerges, highlighting how regulatory ambiguity is influencing long-term investment decisions in Canada’s energy sector. Meanwhile, the firm acquired $765M in natural gas assets from Tourmaline Oil Corp., raised its dividend, and reported $5.3B in Q4 profit, reflecting strong production growth despite softer product revenues.

Weekly Diversion:

Check out this video: Backyard Bunker Build

Charts of the Week

Real assets have moved from the periphery of portfolios to the center of the inflation conversation, and the included charts make clear why. They show that the return experience and inflation sensitivity of different asset classes are far from uniform, with tangible assets behaving very differently than traditional stocks and bonds over the past decade.

The first chart compares one-year total returns and annualized five-year total returns across several asset classes. It shows that natural resources, infrastructure, and commodities have delivered significantly higher one-year returns than traditional U.S. assets like the S&P 500 (large-cap equities), Aggregate Bonds, REITs, and TIPS, while over five years the performance gap between real assets and major asset classes is narrower but still generally more favorable to real assets.

Source: Carson Investment Research, Morningstar

Source: Carson Investment Research, Morningstar

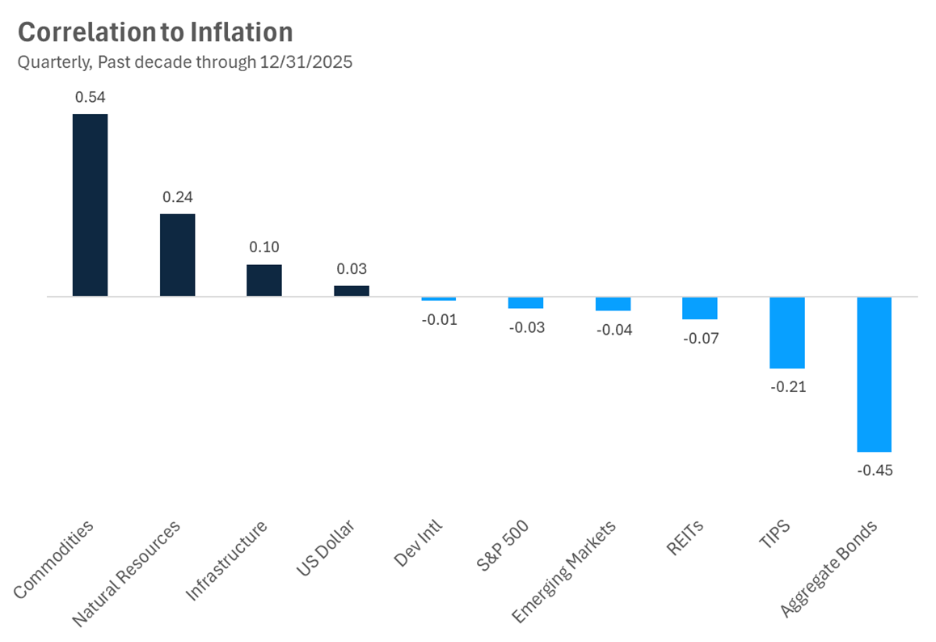

The inflation correlation chart below is particularly revealing. Commodities sit at the top with a strong positive relationship to changes in consumer prices, followed by natural resource companies and infrastructure. This pattern suggests that assets tied directly to the production, processing, and delivery of raw materials tend to benefit when inflation rises, because their revenues and replacement costs are linked to the very prices that are moving higher. By contrast, broad equity benchmarks, developed and emerging international stocks, and listed real estate investment trusts all hover around zero or slightly negative correlation, implying that their short-term experience during inflation shocks can be far less protective than investors often assume.

Source: Carson Investment Research, Morningstar

Source: Carson Investment Research, Morningstar

On the defensive side of the chart above, traditional fixed income shows a pronounced negative correlation to inflation, with aggregate bonds in particular sitting at the bottom. This underscores the mechanical headwind that rising prices and interest rates create for nominal bonds, as discount rates adjust upward faster than coupons can compensate. Even securities explicitly designed to address inflation, such as TIPS, appear only modestly supportive in the data, with a negative—rather than positive—correlation to inflation surprises despite their structural linkage to price levels.

Taken together, the charts argue for thinking about real assets as a distinct building block in portfolio construction rather than a niche satellite. Their differentiated correlation profile suggests they can improve overall resilience when inflation is volatile, especially if they are accessed through a diversified mix of commodities, resource equities, and infrastructure rather than a single precious metal or theme. At the same time, their cyclicality and potential for sharp drawdowns mean they are better used as a diversifying complement to equities and bonds, not a wholesale replacement. The challenge for investors today is to calibrate that allocation thoughtfully, recognizing that the same forces that have recently propelled real assets may also introduce new bouts of volatility as the inflation cycle evolves.

Sources: Yahoo Finance, First Trust, Advisor Analyst, Financial Post, Bespoke Investment Group

©2026 Milestone Wealth Management Ltd. All rights reserved.

DISCLAIMER: Investing in equities is not guaranteed, values change frequently, and past results are not necessarily an indicator of future performance. Investors cannot invest directly in an index. Index returns do not reflect any fees, expenses, or sales charges. Opinions and estimates are written as of the date of this report and may change without notice. Any commentaries, reports or other content are provided for your information only and are not considered investment advice. Readers should not act on this information without first consulting Milestone, their investment advisor, tax advisor, financial planner, or lawyer. This communication is intended for Canadian residents only and does not constitute as an offer or solicitation by anyone in any jurisdiction in which such an offer is not allowed.