Market Insights: Higher Capex, Healthy Buybacks, Steady Flows

Milestone Wealth Management Ltd. - Feb 27, 2026

Macroeconomic and Market Developments:

- North American markets were mixed this week. In Canada, the S&P/TSX Composite Index closed 1.55% higher, while in the U.S., the Dow Jones Industrial Average fell by 1.31% and the S&P 500 Index decreased 0.44%.

- The Canadian Dollar inched up this week, closing at 73.23 vs. 73.12 cents USD last week.

- Oil prices rose again this week, with U.S. West Texas Crude closing at US$67.29 vs. US$66.49 last week.

- The price of Gold rose again this week closing at US$5,281 vs. US$5,115 last week.

- U.S. Producer Price Index (PPI) rose 0.5% in January, above expectations (+0.3%), with headline producer prices up 2.9% y/y. Core PPI (excluding food and energy) climbed 0.8%, its strongest monthly gain since mid-2022, lifting the annual core rate to 3.6%. Notably, energy (-2.7%) and food (-1.5%) declined, while services inflation — particularly wholesale machinery margins — drove much of the increase. Goods prices remain relatively contained (+1.6% y/y), and intermediate input costs were flat to lower. Despite the firm monthly print, underlying money supply growth (M2 +4.3% y/y) and moderating trends suggest inflation pressures may remain contained, potentially leaving room for rate cuts later in 2026

- Canada’s economy contracted 0.6% annualized in Q4 2025, worse than the expected -0.4%, as businesses drew down inventories rather than boosting production. However, underlying demand was firmer than the headline suggests: consumer spending rebounded 1.7% annualized, exports continued recovering, business investment edged higher, and corporate operating surplus rose 1.3%. Full-year 2025 growth came in at 1.7%, the slowest since 2020, with per-capita GDP flat in Q4.

- Canada’s federal deficit widened to $26.14B for April–December FY2025-26, up from $21.72B a year earlier, as program spending rose to $344.9B (from $333.2B) amid higher direct spending and transfers. Revenues increased to $363.4B, supported by stronger personal and corporate tax receipts and higher customs duties tied to countermeasures against U.S. tariffs. Public debt charges edged slightly lower to $40.9B, reflecting reduced short-term rates, while net actuarial losses rose modestly.

- Canada’s Big Six banks delivered a blockbuster Q1, generating roughly $19B in combined profit (up from ~$14B y/y), with all major lenders beating expectations. Royal Bank of Canada earned $5.79B, TD Bank Group $4.04B, CIBC $3.10B, Scotiabank $2.3B, Bank of Montreal $2.49B, and National Bank of Canada $1.25B. Analysts credited disciplined capital management, strong capital markets activity, resilient loan volumes, and moderating credit provisions, though questions remain around limited top-line growth and pockets of elevated mortgage impairments. At the same time, critics note the contrast between bank profitability and a softening labour backdrop — with 35.4K jobs lost in December led by losses in manufacturing, wholesale trade, and transportation and negative job growth in Q4 — arguing that elevated policy rates from the Bank of Canada have supported net interest margins and fee income even as households face higher borrowing costs. For example, Royal’s Personal Banking net income rose 17% y/y, aided by margin expansion as mortgages reprice at higher rates, underscoring how the current rate environment continues to favour large financial institutions despite broader economic strain.

- Australia's inaugural shipment of liquefied natural gas (LNG) to eastern Canada, spanning 16,000 miles, has arrived at a time when China's projected 2025 imports are declining by 11% and Asian demand remains subdued, leading exporters to seek new opportunities in markets like Europe and the Americas. This transaction highlights Canada's ironic situation of importing super-chilled gas despite abundant domestic natural gas reserves, a predicament worsened by delayed pipeline projects and local opposition in provinces such as Quebec and British Columbia. Public responses to the news express significant frustration with the Liberal government's federal policies, emphasizing deep interprovincial energy divisions and advocating for greater domestic resource development to minimize dependence on far-flung imports.

- Paramount Skydance Corp. agreed to acquire Warner Bros. Discovery Inc. for $111B, outbidding Netflix Inc. after a months-long takeover battle. Netflix walked away from its $82.7B offer, citing valuation discipline, while Paramount sweetened its bid by covering a $2.8B termination fee and securing $57.5B in committed debt financing.

Weekly Diversion:

Check out this video: Basically Mini Golfing at This Point

Charts of the Week

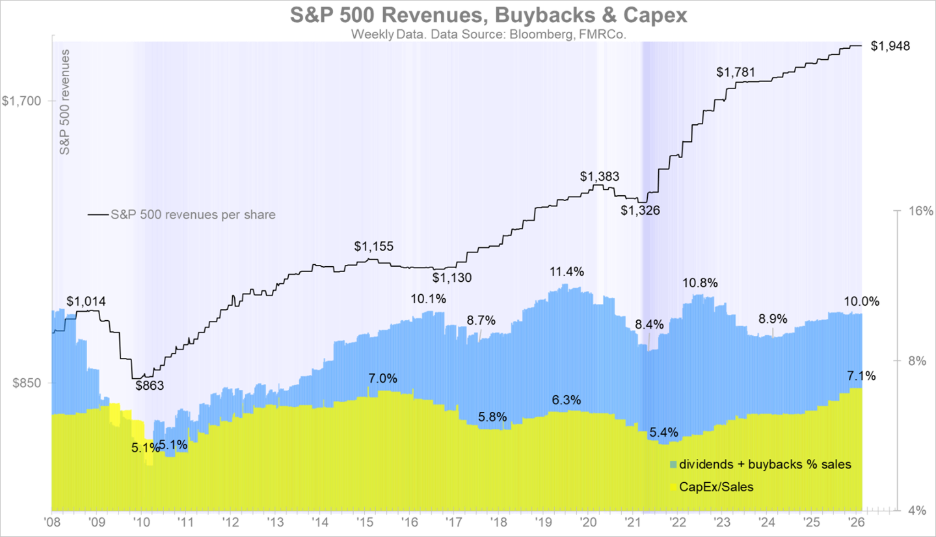

Corporate investment appears to be quietly entering a powerful upswing, reshaping both market leadership and the underlying character of this cycle. The evidence is visible in how much more of each revenue dollar is now being reinvested, yet without sacrificing shareholder distributions.

One central driver is that spending on physical and intangible assets has accelerated faster than sales themselves, lifting capital expenditure intensity from the low single digits of revenue to materially higher levels. Because revenues per share have also climbed substantially over the last forty months, the result is that investment per share has effectively doubled, signalling a regime shift rather than a modest tweak in budgeting. As highlighted in the first chart, this combination of higher margins, larger revenue bases, and rising reinvestment rates is characteristic of an expansion phase in the corporate profit and productivity cycle.

Source: Bloomberg, FMRCo, via Fidelity Investments

Source: Bloomberg, FMRCo, via Fidelity Investments

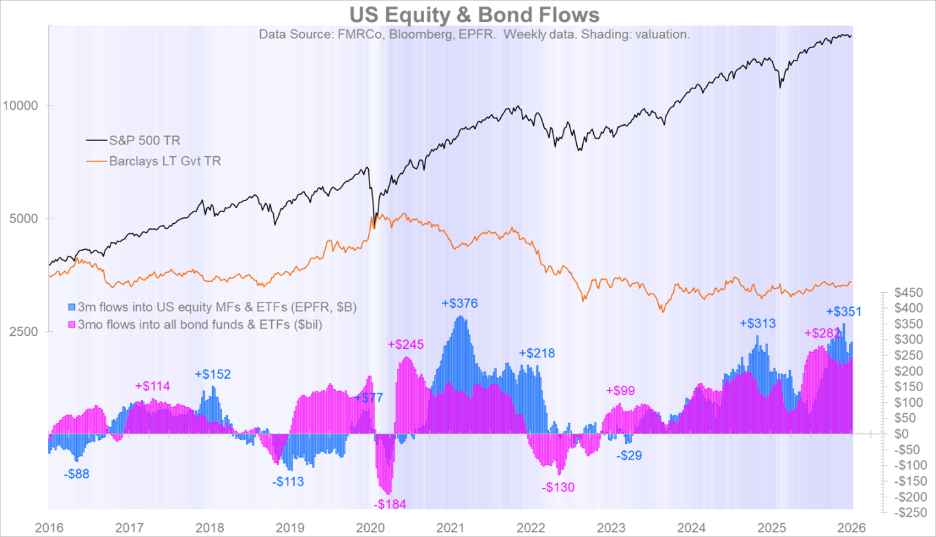

Money flow data also seems to reinforce the idea that this is a broad, durable cycle rather than a narrow, late stage blowoff. In the next chart of U.S. equity and bond fund flows, multi-year episodes of large net inflows into both risk assets and fixed income sit alongside rising total returns for equity indices and long-term government bonds, implying that long horizon investors remain comfortable adding exposure across the capital structure. The sequence of annual flow bars—swinging from sizable outflows in years of stress to record inflows more recently—underscores how repositioning has moved from de-risking to re-risking as macro uncertainty has faded and earnings visibility improved. Persistent positive flows into both equities and bonds also mitigate the usual concern that rising capex must crowd out shareholder returns, since there is ongoing external demand to absorb new issuance and support valuations.

Source: FMRCo, Bloomberg, EPFR, via Fidelity Investments

Source: FMRCo, Bloomberg, EPFR, via Fidelity Investments

Taken together, the charts portray a market in which companies are committing more cash to long-term projects while investors are steadily supplying capital. Rather than a fragile boom dependent on a single story, the emerging capex cycle appears to rest on thicker profit cushions, healthier balance sheets, and a more measured risk appetite. If these trends persist, the payoff is likely to be a period where productivity gains, earnings durability, and shareholder distributions can co-exist, even as the investment share of corporate income continues to rise.

Sources: Yahoo Finance, First Trust, Bloomberg, CTV, Global, @drJstrategy, Canadian Press, Financial Post, FMRCo, Bloomberg, EPFR, Fidelity Investments

©2026 Milestone Wealth Management Ltd. All rights reserved.

DISCLAIMER: Investing in equities is not guaranteed, values change frequently, and past results are not necessarily an indicator of future performance. Investors cannot invest directly in an index. Index returns do not reflect any fees, expenses, or sales charges. Opinions and estimates are written as of the date of this report and may change without notice. Any commentaries, reports or other content are provided for your information only and are not considered investment advice. Readers should not act on this information without first consulting Milestone, their investment advisor, tax advisor, financial planner, or lawyer. This communication is intended for Canadian residents only and does not constitute as an offer or solicitation by anyone in any jurisdiction in which such an offer is not allowed.